Key Takeaways

- Prioritize building and maintaining excellent credit scores (700+).

- Get pre-approved by various lenders, especially credit unions, before visiting dealerships.

- Understand and manage your debt-to-income (DTI) ratio.

- Be prepared to make a significant down payment to reduce the loan amount and interest.

- Rate shop aggressively within a 14-45 day window to minimize credit impact.

- For thin files, an authorized user tradeline may provide near-term credit visibility support, but always pair it with durable long-term credit building.

Understanding the Lender's Perch: What Banks Look For

When you approach a lender for a car loan, they're essentially evaluating the stability of your financial 'nest.' They want to know you're a responsible borrower who will honor your commitment. Your credit score is the most immediate indicator of this, but it’s far from the only factor. Lenders look at several key elements to determine your eligibility and, critically, your interest rate.

Debt-to-Income (DTI) Ratio

A financial metric that compares your total monthly debt payments to your gross monthly income, indicating how much of your earnings are already committed.

Lenders also consider your employment history, ensuring a stable income source, and your overall credit history, the longer your positive track record, the better. They want to see a diverse mix of credit, such as credit cards and perhaps a previous installment loan, which demonstrates your ability to manage different types of credit responsibly. Every piece of your financial story helps them form a complete picture.

The Power of Pre-Approval: Your Negotiation Wingman

One of the most potent strategies for securing a low-interest car loan is pre-approval. This isn't just a suggestion; it's a foundational step that empowers you with negotiating leverage. When you get pre-approved, a lender evaluates your credit and financial situation and offers you a specific loan amount at a set interest rate before you even set foot in a dealership. This transforms your car-buying experience from a frantic scramble to a confident, informed decision.

Imagine you're trying to choose the smoothest branch for your next migration. If you arrive at the dealership armed with a pre-approval letter, you're no longer dependent on their financing options. You know exactly what interest rate you qualify for elsewhere. This allows you to treat the dealership's financing offer as just another quote to compare. If they can beat your pre-approved rate, great! If not, you already have a fantastic alternative. This crucial step prevents you from being cornered into higher rates simply because you didn't have a benchmark.

Credit unions, in particular, are often excellent sources for low-interest car loans. As member-owned institutions, they frequently offer more competitive rates and personalized service compared to larger banks. It’s always wise to check with local credit unions, even if you’re not currently a member, as many have open membership policies.

Rate Shopping Like a Pro: Mastering the "Soft Pull" Flight Path

Think of it as scouting multiple strong branches for your nest before you commit. Each offer gives you valuable data, allowing you to choose the absolute best interest rate. Don't simply accept the first offer, even if it seems good. A difference of just half a percentage point can save you hundreds, or even thousands, of dollars over the life of the loan. This is especially true with car loans, which often have shorter terms than mortgages, making every fraction of a percent more impactful on your monthly payment and total cost.

A common confusion at this stage is whether applying broadly will automatically punish your score.

"Applying with multiple auto lenders always hurts your score multiple times."

Auto-loan inquiries in the same short shopping window are typically grouped for scoring.

Why?

Keep applications focused on serious quotes and complete them inside one 14-45 day rate-shopping window.

Use this sequence to keep comparison disciplined and lender-friendly:

Collect baseline offers

Start with one bank and one credit union pre-approval.

Expand lender set

Add online lenders inside the same shopping window.

Normalize comparisons

Align term, down payment, and fees before choosing.

Negotiate at dealership

Use your best outside offer as the benchmark.

The Broader Landscape of Your Credit Profile: Beyond the Score

While your credit score is the headline, the entire story of your credit report paints a more comprehensive picture for lenders. They'll delve into the details:

- Payment History: This is the most significant factor, accounting for about 35% of your FICO score. A pristine record of on-time payments across all your accounts is paramount. Even one missed payment can significantly ding your score and raise red flags for potential lenders. See how payment history drives your score.

- Length of Credit History: The longer your positive credit history, the better. It demonstrates a sustained ability to manage credit over time. Closing old accounts can sometimes be detrimental because it shortens your average account age. See when closing old cards can backfire.

- Credit Mix: Having a healthy mix of revolving credit (like credit cards) and installment credit (like previous student loans or personal loans) shows you can handle different types of debt responsibly. This factor, while less impactful than payment history or utilization, still contributes to a robust credit profile. Use this revolving vs. installment framework.

- New Credit: While rate shopping for a car loan is understood, opening too many new accounts just before applying for a major loan can make you appear risky. Lenders might see you as desperate for credit, or as someone taking on more debt than you can handle.

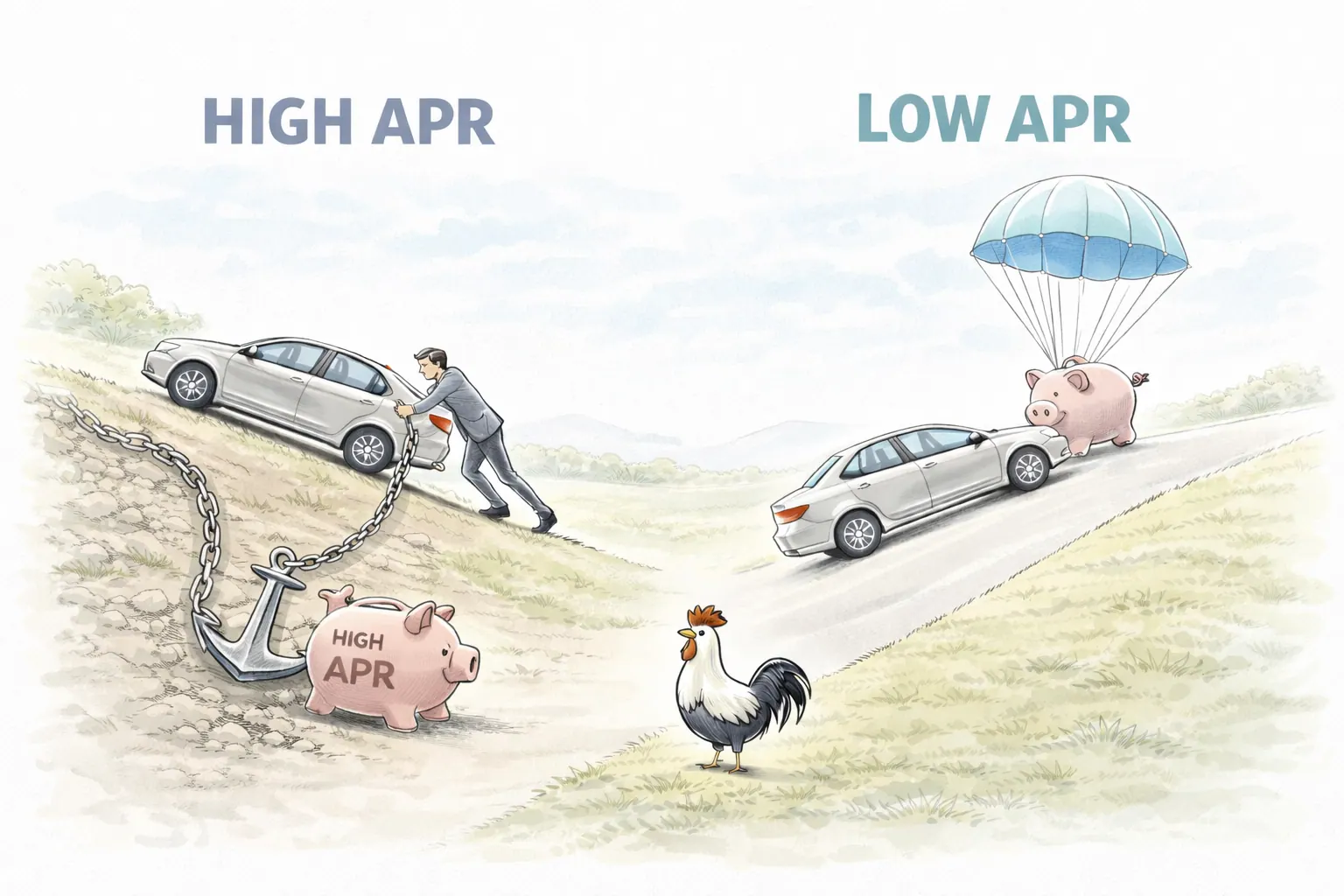

Beyond your credit report, other financial decisions impact your loan. A sizeable down payment immediately reduces the loan amount, which in turn reduces the lender's risk and the total interest you'll pay. A larger down payment can also help you secure a lower interest rate, as it demonstrates your commitment and reduces the loan-to-value (LTV) ratio of the vehicle. Similarly, choosing a shorter loan term (e.g., 36 or 48 months instead of 60 or 72 months) often results in a lower interest rate, though it means higher monthly payments. While a longer term makes monthly payments more affordable, it often leads to paying significantly more in interest over the life of the loan and increases the risk of being upside down on your loan (owing more than the car is worth).

A Strategic Boost: When a Tradeline Can Help

If you use an AU tradeline before financing, execution quality matters more than speed alone.

AU Tradeline Use Before Auto Financing

- Choose seasoned accounts with long positive history and low utilization.

- Confirm timing so the account can report before underwriting.

- Pair AU support with your own active accounts and on-time payments.

- Rely on AU data as a standalone long-term credit strategy.

- Add multiple uncertain tradelines right before loan applications.

- Assume every lender weights AU accounts the same way.

Handled correctly, this support may improve near-term visibility while you keep building durable credit in your own name.

Real-Life Journeys to Lower Rates

These stories illustrate how strategic planning can lead to significant savings:

- Nico's First Car Loan: Nico, a recent college graduate, had a good credit score (720) but a thin file with only one student loan and a single credit card. When looking for a car, he felt his offers were okay but not great. He decided to pursue pre-approval from a local credit union and an online lender. The credit union, seeing his potential, offered a rate almost a full percentage point lower than the dealership. Nico also made a 15% down payment, which further sweetened the deal, showing lenders his commitment. He secured a 48-month loan at a fantastic rate, illustrating how a focused approach can beat dealer financing.

- Riley's Rebound Car Purchase: Riley had rebuilt his credit after a few tough years, now boasting a solid 745 score. However, his debt-to-income (DTI) was slightly higher than optimal due to student loans and a mortgage. Before applying, Riley diligently paid down one of his credit cards to almost zero, improving his utilization and giving his score a small bump. He then got pre-approved by three different lenders over two weeks. He found that one online lender offered the most competitive rate, significantly better than the dealership’s initial offer. Riley's proactive DTI management and strategic rate shopping paid off, saving him a substantial amount over the loan's term.

- The Time-Sensitive Vehicle: Maria needed a reliable car quickly after her old vehicle unexpectedly broke down. With a 760 credit score, she knew she qualified for excellent rates. Instead of rushing to a dealership, she spent a single afternoon online, applying for pre-approval with two credit unions and her personal bank. Within hours, she had two strong offers. Armed with the best one, she visited a dealership, confident in her financing. When the dealer tried to offer a higher rate, she politely presented her pre-approval, and they immediately matched it to secure her business, demonstrating the power of pre-approval even when time is tight.

Your Flight Plan: Steps to Secure Your Low-Interest Loan

Getting the best possible car loan rate requires diligence and a clear strategy. Here’s a concise plan to guide your journey:

- Know Your Score: Obtain your credit scores (FICO preferred by auto lenders) from all three bureaus well in advance via free annual credit reports. Correct any errors you find using this reporting guide and this dispute process.

- Optimize Your Profile: Pay down credit card balances to lower your utilization ratio, ensure all payments are on time, and avoid opening new credit accounts for at least 3-6 months before applying.

- Get Pre-Approved (Crucial Step): Apply to multiple lenders, especially credit unions, national banks, and online lenders, to get a benchmark rate. Do this within a short window (14-45 days) to minimize credit score impact.

- Calculate Your DTI: Understand your current debt-to-income ratio and see if there are any debts you can pay down to improve it before applying.

- Save for a Down Payment: The more you put down, the less you borrow, which usually translates to a lower interest rate and reduces your total cost.

- Consider Loan Term: Balance monthly payment affordability with the total interest paid. Shorter terms often yield lower rates.

- Be Ready to Negotiate: Use your pre-approval to negotiate with the dealership's finance department. They may try to beat your outside offer.

Remember, the goal isn't just to get a car loan, but to secure the most favorable terms possible for your financial well-being.

Building Your Durable Vehicle Nest: Long-Term Credit Health

Securing a low-interest car loan is a testament to strong credit, but it's also an opportunity to reinforce your overall financial nest. This new installment loan, with consistent on-time payments, can further diversify your credit mix and may positively impact your payment history, two pillars of a robust credit profile. For those still building or rebuilding their credit, remember that while an Authorized User tradeline can offer a fast gateway to credit visibility, true, durable strength comes from adding your own accounts. Consider pairing any tradeline strategy with proven builders like secured credit cards, credit-builder loans, and rent reporting. These tools help you weave the strong, resilient branches that support your financial future, well beyond the life of your car loan. Your commitment to these habits supports a stronger foundation for future financial milestones.

Ready to assess your credit health or explore tools that can help you secure better loan terms? We're here to help you understand your options.

Action Items

Before you sign, verify how your target lender treats AU accounts and confirm your final terms against your pre-approval benchmarks.

Discloure

Some lenders and credit scoring models may filter out, discount, or weigh authorized user tradelines differently in their underwriting decisions. Results vary based on lender policies, the specific scoring model used, and your unique credit profile. An AU tradeline does not guarantee loan approval or any specific credit score outcome.

For a quick benchmark while comparing offers, use this directional APR view:

Typical Auto APR Bands by Credit Range

| Credit range | Typical APR band | Negotiation posture |

|---|---|---|

| 760+ (Excellent) | 3% - 5% | Press for top-tier lender pricing |

| 700-759 (Good) | 5% - 8% | Leverage multiple pre-approvals |

| 660-699 (Fair) | 8% - 12% | Prioritize structure and total cost |

Treat these ranges as directional context, then decide based on your actual term, fees, and total repayment cost.

Frequently Asked Questions

1. How much does my credit score affect car loan rates?

- Your credit score is a primary factor. A higher score (generally 700+ FICO) signals less risk to lenders, leading to significantly lower interest rates. Scores below 600 often result in much higher rates or require co-signers. The difference between 'good' and 'excellent' credit can save you hundreds, if not thousands, of dollars over the life of the loan.

2. What is a good interest rate for a car loan?

- What constitutes a 'good' interest rate varies based on your credit score, the current economic climate, and the loan term. For borrowers with excellent credit (760+), rates can be as low as 3-5% (or even lower during promotional periods). With good credit (700-759), you might see rates in the 5-8% range. It's always best to compare multiple offers to determine what's competitive for your specific situation.

3. Should I get pre-approved before going to the dealership?

- Absolutely. Pre-approval from a bank, credit union, or online lender gives you a benchmark loan offer. This empowers you to negotiate with the dealership from a position of strength, either accepting their better offer or using your pre-approval. It ensures you don't overpay for financing.

4. Can a large down payment lower my interest rate?

- Yes, a larger down payment typically lowers your interest rate. By reducing the amount you need to borrow, you decrease the lender's risk. This makes you a more attractive borrower and can qualify you for better terms. It also reduces your monthly payments and the total amount of interest you'll pay over the loan's life.

5. How long should my car loan term be?

- The ideal car loan term balances monthly affordability with total interest paid. Shorter terms (e.g., 36-48 months) generally come with lower interest rates but higher monthly payments. Longer terms (e.g., 60-72 months) offer lower monthly payments but accumulate more interest over time and increase the risk of being 'upside down' on your loan. Choose the shortest term you can comfortably afford.

6. Does applying for multiple car loans hurt my credit?

- Credit bureaus recognize that consumers shop for the best loan rates. Multiple inquiries for the same type of loan (like an auto loan) within a short window (typically 14 to 45 days, depending on the scoring model) are usually treated as a single hard inquiry for scoring purposes. This allows you to rate shop confidently without significant cumulative damage to your score.

7. When should I consider an Authorized User tradeline for a car loan?

- An Authorized User (AU) tradeline can be considered if you have a 'thin' credit file (not much history) but an otherwise clean record, and you need near-term support for credit visibility before applying for a car loan. It can add positive payment history and credit limits to your report, potentially improving your score. However, it's a gateway for visibility, and for durable credit strength, it must be combined with building your own credit accounts like secured cards or credit-builder loans.

Like building a sturdy nest, securing a low-interest car loan is an investment in stability. When you understand what lenders evaluate, prepare your profile, and rate shop with discipline, you make decisions that protect your cash flow for years. With careful planning, you can leave with the car you need and the confidence that your financing terms are working for you.