Key Takeaways

- FICO models consolidate multiple inquiries for specific loan types (mortgage, auto, student) if made within a 'shopping window'.

- This window typically ranges from 14 to 45 days, depending on the scoring model used.

- The rule helps you compare loan offers and secure the best rates without fear of significant, repeated credit score drops.

- It primarily applies to installment loans, not revolving credit like credit cards.

- Preparation is key: know your credit score and debt-to-income ratio before you begin shopping.

The Hard Inquiry Dilemma, Revisited

on a 30-year mortgage from 0.5% lower rate

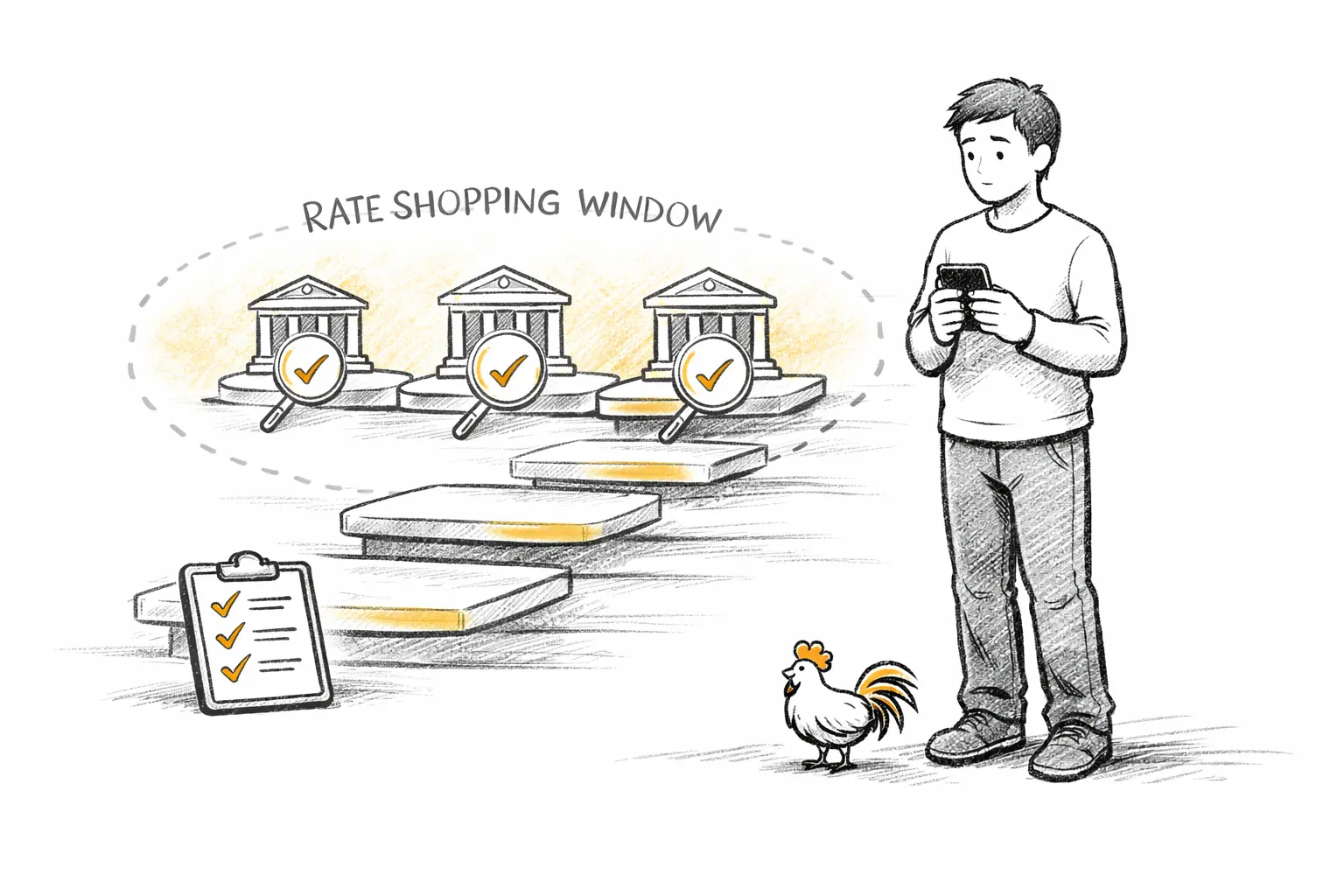

The Rate Shopping Rule: A Savior for Your Score

Rate Shopping Rule

A FICO rule allowing multiple hard inquiries for the same type of installment loan (e.g., mortgage, auto, student) within a specific timeframe (typically 14-45 days) to be treated as a single inquiry for scoring purposes.

The Magic "Shopping Window"

"Applying to multiple lenders destroys your credit score."

Rate shopping within 14-45 days counts as a single inquiry.

Why?

FICO designed this rule specifically to encourage consumers to shop for the best rates on major purchases.

Day 1

Apply for first loan quote

Day 7

Visit 2-3 more lenders

Day 14

Review all offers received

Day 21

Select best rate (1 inquiry total)

Why This Rule Matters for Your Nest Egg

Hard inquiries affect the "New Credit" category, which accounts for only 10% of your FICO score. This limited impact is precisely why the Rate Shopping Rule can protect you: consolidating multiple inquiries keeps this factor from being disproportionately affected.

Real-Life Scenarios: Birds Applying the Rule

Let's imagine some birds applying this rule to their own nests:

Identify your loan type (mortgage, auto, student)

Research 3-5 lenders with competitive rates

Submit all applications within 14-45 days

Compare APR, fees, and terms side-by-side

Choose the best offer (only 1 inquiry counted!)

-

Newcomer Nico, the Car Buyer: Nico, a young bird just starting to build their independent credit history, needs a reliable car to get to work. They are nervous about applying for an auto loan because they have heard about hard inquiries. Understanding the Rate Shopping Rule, Nico spends a weekend visiting three different dealerships and two local credit unions, getting pre-approved for an auto loan at each (learn why building credit visibility first can help you qualify). Because all these applications happen within a 30-day window, FICO treats them as a single search for a car loan. Nico gets to compare the best rates, chooses the most favorable terms, and only sees one temporary ding on their credit score, not five.

-

Rebuilder Riley, the Refinancer: Riley had some financial storms in the past but has diligently rebuilt their credit nest over the years. Now, with a significantly improved credit score, Riley wants to refinance their mortgage to a lower interest rate. Knowing that small differences in mortgage rates can save tens of thousands of dollars, Riley contacts four different mortgage lenders and a mortgage broker over two weeks. Each lender pulls Riley's credit report. Thanks to the Rate Shopping Rule (and by preparing thoroughly before applying, as outlined in Preparing for a Mortgage), these multiple inquiries are consolidated into one for FICO scoring purposes. Riley secures an excellent new rate, significantly reducing their monthly payments and further strengthening their financial foundation.

-

Time-Sensitive Stella, the Student: Stella needs to secure a private student loan to cover tuition quickly for the upcoming semester. She researches two different banks and an online lender. Within a 10-day period, she submits applications to all three to compare offers. Because these are student loans and fall within the shopping window, her credit score registers these efforts as one inquiry, allowing her to focus on comparing the terms without worrying about unnecessary credit damage.

Auto Loans

Rate shopping applies

Mortgages

Rate shopping applies

Student Loans

Rate shopping applies

Credit Cards

Each inquiry counts separately

Beyond the Window: Other Factors to Consider

Once you understand this distinction, you can use rate shopping strategically. You will know exactly when this protection applies and when it does not.

Are you rate shopping for a mortgage, auto loan, or student loan?

Nest-Building Strategy: Using the Rule to Your Advantage

- Complete all applications within 14-45 days

- Apply for the SAME type of loan only

- Review your credit report first

- Compare APR, fees, and terms

- Apply for different loan types together

- Spread applications over months

- Forget to check for pre-qualification offers

- Accept the first offer without shopping

Preparing properly before you start shopping can make the difference between qualifying for excellent rates and settling for mediocre terms. Here is your action checklist:

Action Items

Frequently Asked Questions

1. What is the Rate Shopping Rule?

- The Rate Shopping Rule is a FICO credit scoring guideline that allows multiple hard inquiries for the same type of installment loan (like a mortgage, auto, or student loan) within a specific timeframe (usually 14-45 days) to be counted as a single inquiry. This helps consumers compare loan offers without excessive damage to their credit score.

2. How long is the "shopping window" for the Rate Shopping Rule?

- The shopping window typically ranges from 14 to 45 days, though the exact duration can vary slightly depending on the specific FICO scoring model used and the credit bureau.

3. Which types of loans does the Rate Shopping Rule apply to?

- It primarily applies to installment loans such as mortgages, auto loans, and student loans. It generally does not apply to revolving credit accounts like credit cards or personal lines of credit.

4. Will applying for multiple loans still temporarily lower my credit score?

- Yes, your credit score might still experience a small, temporary dip from the first hard inquiry. However, subsequent inquiries for the same type of loan within the shopping window will not cause additional drops, as they are consolidated into one for scoring purposes.

5. What happens if I apply for different types of loans within the shopping window?

- The Rate Shopping Rule applies only to inquiries for the same type of loan. If you apply for a mortgage and an auto loan within the same window, they will likely be treated as two separate inquiries, each potentially causing a small, temporary score drop.

6. Why is it important to "rate shop" for loans?

- Rate shopping allows you to compare interest rates, fees, and terms from multiple lenders, which can save you potentially thousands of dollars over the life of a major loan. The Rate Shopping Rule ensures you can do this without being unfairly penalized for being a diligent consumer.

7. Does the Rate Shopping Rule prevent new accounts from impacting my credit?

- No, the rule only protects against multiple inquiry hits for the same loan type. Opening a new account will still impact other factors of your credit score, such as the average age of your accounts and your credit mix.

By understanding how the Rate Shopping Rule works, you can turn a common credit fear into a massive opportunity. You don't have to be afraid of exploring your options or comparing lenders. Instead, you can move forward as an informed, confident consumer, gathering the best possible terms for your financial home. This strategic approach ensures you secure the most favorable rates, strengthening your financial foundation for years to come.

Depends on FICO model version

Discloure

Some lenders and credit scoring models may filter out, discount, or weigh authorized user tradelines differently in their underwriting decisions. Results vary based on lender policies, the specific scoring model used, and your unique credit profile. An AU tradeline does not guarantee loan approval or any specific credit score outcome.