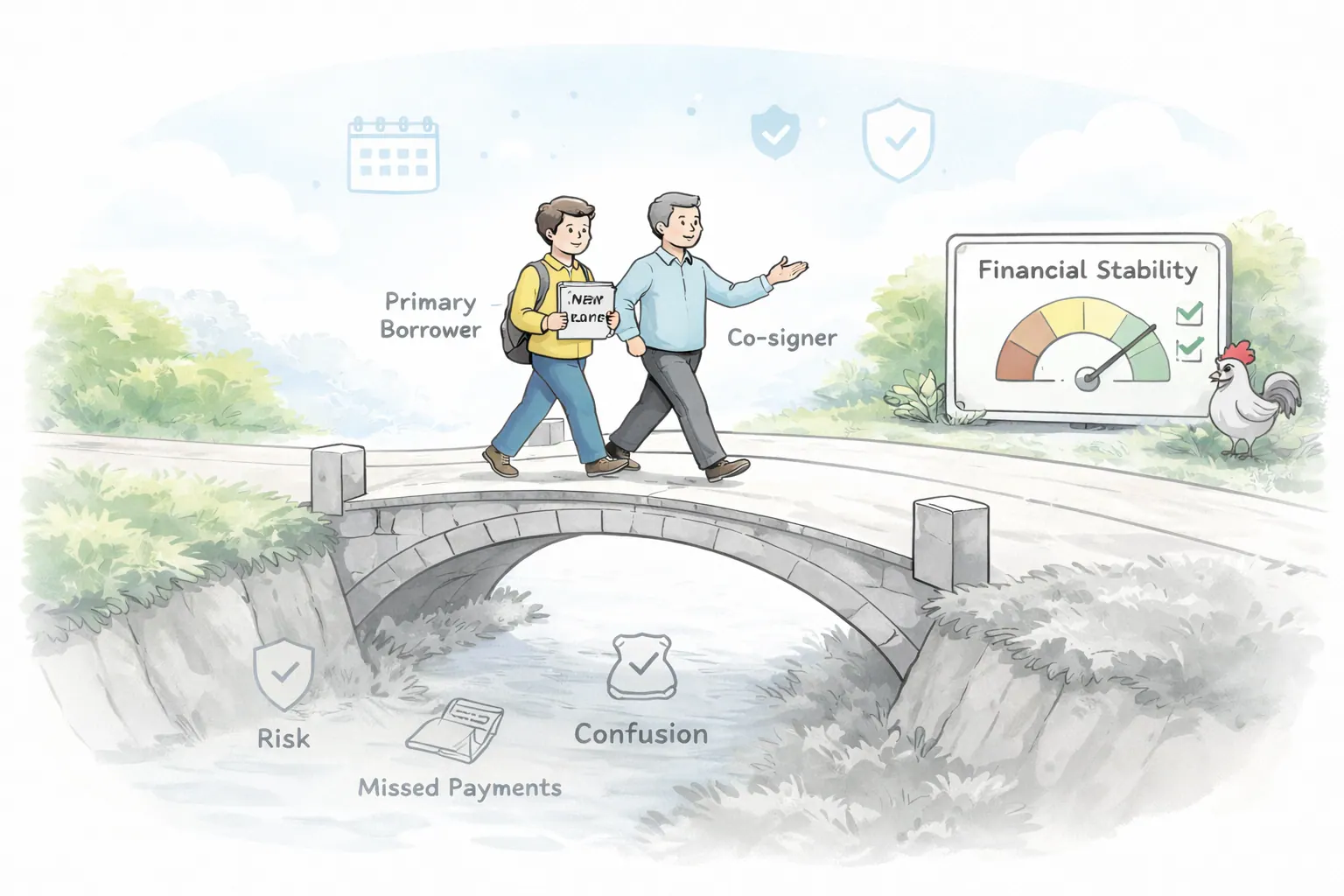

Key Takeaways

- A cosigner legally shares responsibility for the loan, helping you qualify by adding their strong credit profile.

- This is a high-trust arrangement; missed payments will negatively impact both your credit scores and the cosigner's.

- While a cosigned loan builds your credit, pair it with personal efforts like secured cards or credit-builder loans for durable financial independence.

- Open communication and a clear payment plan are essential for protecting both your credit and your relationship.

- A cosigned loan helps establish a positive tradeline, but it's a stepping stone, not the final destination, in your credit-building journey.

The Benefits of a Cosigned Loan for Your Emerging Nest

The most significant benefit of having a cosigner, especially for a first-time applicant, is the ability to actually qualify for a loan in the first place. Without an established credit history, many doors to credit remain closed. A cosigner can unlock those doors, allowing you to secure necessary financing for things like:

- A Car Loan: Crucial for transportation to work or school. If this is your immediate goal, review how lenders price low-interest car loans.

- A Personal Loan: Perhaps to consolidate high-interest debt (if you're a rebuilder) or cover an essential expense.

- A Student Loan: To fund your education and invest in your future. For repayment strategy and score impact, see how student loans affect your credit profile.

Beyond simply qualifying, a cosigner's strong credit profile can also lead to better loan terms. Lenders often offer lower interest rates and more favorable repayment schedules to borrowers who present less risk. You could save hundreds or even thousands of dollars over the life of the loan, allowing more of your financial 'eggs' to stay in your nest.

Crucially for our topic, a cosigned loan is one way to build your own credit history. When the loan is approved, it appears on both your credit report and your cosigner’s report. As you make consistent, on-time payments, this payment history is reported to the major credit bureaus. This establishes a tradeline on your credit file, your very first sturdy branch in your credit nest. Each on-time payment demonstrates your reliability and financial responsibility, which are key pillars of a strong credit score. Over time, this history helps you build an independent track record of your own — how lenders weigh it is up to them.

Tradeline

An account that appears on your credit report, representing a line of credit (like a credit card or loan) and its payment history. It's a fundamental building block of your credit profile.

The Risks of a Shared Nest: A Word of Caution

While incredibly helpful, a cosigned loan isn't without its potential storms. It’s essential to understand the risks involved, not just for you but especially for your cosigner. This isn't just a friendly gesture; it’s a legally binding agreement with significant financial implications for both parties.

For the Cosigner:

- Full Legal Responsibility: The cosigner is just as responsible for the loan as you are. If you miss a payment, they are legally obligated to make it. If you default entirely, the lender will pursue them for the full amount.

- Credit Score Impact: Every payment, whether on time or missed, is reported on their credit report too. A single late payment on your cosigned loan can damage their excellent credit score, potentially affecting their ability to secure their own loans or favorable rates in the future.

- Debt-to-Income Ratio: The loan amount will be factored into their DTI ratio, even if you’re making all the payments. This could make it harder for them to qualify for their own mortgages, car loans, or other credit in the future.

- Strained Relationships: Financial disagreements or unexpected payment issues can put immense stress on personal relationships, potentially damaging bonds of trust that are difficult to rebuild.

For the Borrower (You):

- Immense Responsibility: You have an ethical and legal obligation to protect your cosigner's credit. This means making every single payment on time, without fail. Your financial choices directly impact someone else's financial well-being.

- Damage to Your Own Credit: While a cosigned loan can build your credit, missed payments will just as quickly damage it. And because the loan is on both your reports, you'll still feel the sting. If you want the scoring mechanics, revisit why payment history carries the most weight.

- Loss of Independence: Until you can refinance the loan into your name alone, or pay it off, you remain financially tied to your cosigner for this particular debt.

"If I miss one payment, only my score drops."

A missed payment can hurt both borrower and cosigner credit files.

Why?

Because the same loan is reported on both reports, late payments can damage two profiles at once and create relationship stress.

Before embarking on a cosigned loan, both you and your potential cosigner must have a frank, open conversation about these risks. It's about protecting both your financial futures and the personal trust that makes this arrangement possible.

Weaving Your Own Credit History: Beyond the Cosigner

A cosigned loan is an excellent foundational branch for your credit nest, providing that initial lift. But just as a young bird eventually learns to gather its own twigs, your goal should be to build your own independent credit history so you don't always need a cosigner. A cosigned loan is a stepping stone, not a permanent solution.

Here’s how you can proactively weave your own strong credit history alongside or after your cosigned loan:

- Secured Credit Cards: These cards require a cash deposit, which typically becomes your credit limit. Because the risk to the lender is minimal, they are easier to obtain for those with thin or poor credit. Use it responsibly (keep utilization low, pay on time) to build a positive payment history.

- Credit-Builder Loans: Offered by some credit unions and community banks, these loans work in reverse. The money is held in a savings account while you make payments. Once paid off, you get the money, and the positive payment history is reported.

- Rent Reporting: Services exist that can report your on-time rent payments to credit bureaus, turning a regular monthly expense into a credit-building asset.

Open your first builder account

Start with a secured card or credit-builder loan in your own name.

Protect payment consistency

Use autopay and keep balances controlled to avoid setbacks.

Build independent depth

Add a second responsible account only if cash flow is stable.

Plan your exit from cosigner support

Refinance or pay down enough to remove shared dependency.

It's also worth noting that an Authorized User (AU) tradeline can be another fast gateway to establishing credit visibility. While different from a cosigner (an AU is not legally responsible for the debt), being added as an authorized user to someone else's well-managed credit card account may add positive payment history and account age to your credit report. This can be a strategic move to get initial visibility, which you then reinforce with your own accounts like a secured card or credit-builder loan. Some lenders may filter or discount AU tradelines during underwriting, so outcomes often depend on lender policy and scoring model. The key is combining these gateway strategies with durable builders for sustainable growth. No single tool guarantees success, but a combination builds the most resilient nest.

Discloure

Some lenders and credit scoring models may filter out, discount, or weigh authorized user tradelines differently in their underwriting decisions. Results vary based on lender policies, the specific scoring model used, and your unique credit profile. An AU tradeline does not guarantee loan approval or any specific credit score outcome.

Mini-Stories: Building Diverse Nests

Let’s look at a few scenarios where cosigners helped first-time applicants take flight:

-

Nico's First Flight: Nico, fresh out of high school, landed his first full-time job and needed a reliable car to get there. He had no credit history whatsoever. His local bank denied his loan application due to his "thin file." His Uncle Marco, who had excellent credit and a stable income, offered to cosign a modest car loan. They had a frank conversation about expectations and a clear agreement: Nico would set up automatic payments from his checking account, and Uncle Marco would monitor his own credit report periodically. For 18 months, Nico made every payment on time. The positive tradeline from the car loan was quickly building his credit score. After a year, Nico successfully applied for his own secured credit card, depositing $200. The cosigned loan gave him the necessary lift to start building his own financial independence.

-

Riley's Rebuilding Roost: Riley had made some missteps with credit in their early twenties, resulting in a few late payments that dinged their score. Now in their late twenties with a stable job, Riley wanted to get a personal loan to consolidate some remaining smaller debts and rebuild their credit. Lenders were still hesitant, offering high interest rates due to their past. Riley’s sister, witnessing their commitment to change, agreed to cosign a small personal loan. This allowed Riley to get a much lower interest rate. With the pressure of a cosigner, Riley was meticulously careful, making every payment on time. The positive tradeline helped demonstrate a new pattern of financial reliability, slowly helping to mend their credit history. The cosigned loan became a crucial tool in rebuilding their roost, showing lenders they could be trusted again.

-

Tara's Academic Ascent: Tara was accepted into her dream university but needed a student loan to cover tuition. At 18, she had no credit history to speak of. Her parents, understanding the investment in her future, cosigned her student loans. They all sat down to discuss the repayment plan and the long-term commitment. Tara understood that these loans would affect her parents' credit for years to come. Throughout college, she worked part-time, saving money to make early payments when possible and preparing herself for the day she would take over full responsibility. The cosigned student loan allowed her to pursue her education, and the on-time payments began the slow, steady process of building her own credit profile from scratch.

Making the Cosigner Conversation Work: Stronger Branches

If you're considering asking someone to cosign for you, or if you're thinking of cosigning for someone, approaching the situation with clarity and respect is paramount. This isn't just about financial numbers; it's about trust and relationships.

Use a simple decision gate before discussing details:

Can the borrower reliably cover the monthly payment from current income?

Once this gate is clear, align on execution details:

- Choose Wisely: For the borrower, select a cosigner who has a strong credit history and stable financial situation, and importantly, someone you have an unwavering trust with. For the potential cosigner, ensure you have a complete picture of the borrower's financial habits and a strong belief in their ability to repay.

- Open Communication is Key: Sit down together and discuss everything. What is the loan for? How will payments be made? What's the plan if one of you faces financial hardship? What are the potential impacts on the cosigner's credit? Don't leave any questions unasked.

- Create a Clear Payment Plan: Detail who is responsible for making payments, how they will be made (e.g., automatic transfers), and what communication will look like. Will the borrower provide proof of payment? How often will statements be reviewed?

- Consider an Exit Strategy: Discuss how the borrower plans to eventually take over the loan independently. This might involve refinancing the loan into their own name once their credit improves, or simply paying off the loan in full. Having this plan in place provides peace of mind for both parties.

- Monitor Credit Reports: Both the borrower and the cosigner should regularly monitor their credit reports. This allows you to catch any errors or missed payments immediately, preventing long-term damage.

Your Flight to Financial Independence

A cosigned loan can be an incredibly effective and strategic first step for building credit, offering a powerful assist when your own financial nest is still taking shape. It provides the crucial tradeline needed to enter the credit landscape and begin demonstrating your reliability.

Ready to explore other ways to build your credit? While a cosigner can provide a powerful start, remember to explore complementary tools like authorized user tradelines for initial visibility, and then secured credit cards or credit-builder loans to build your own strong financial nest. At Credit Roost, we're here to help you find the right tools for a solid foundation and a resilient financial future.

Just like that young bird who eventually learns to soar independently, using the initial support from an experienced elder, you too can transform the opportunity of a cosigned loan into the springboard for your very own, magnificent financial roost. Build wisely, communicate openly, and fly with confidence.

Action Items for a Successful Cosigned Loan

Frequently Asked Questions

-

What exactly is a cosigner in the context of a loan?

- A cosigner is an individual who legally agrees to share responsibility for a loan. They add their strong credit history and income to your application, acting as a guarantee to the lender that the loan will be repaid, even if you, the primary borrower, cannot.

-

How does having a cosigner help me build my own credit?

- When a loan is cosigned, it appears on both your and the cosigner's credit reports. As you make consistent, on-time payments, this positive payment history is reported to the credit bureaus, establishing a positive tradeline on your credit file and demonstrating your financial reliability, which helps build your credit score.

-

What are the primary risks for the cosigner?

- The cosigner bears full legal responsibility for the loan if you default, meaning they'll have to make payments. Missed payments will negatively impact their credit score, and the loan amount will factor into their Debt-to-Income ratio, potentially affecting their ability to secure future credit.

-

Can a cosigner be removed from a loan once my credit improves?

- Often, yes, but it depends on the lender and loan terms. The most common ways are to refinance the loan solely in your name once your creditworthiness is sufficient, or to pay off the loan in its entirety. Some lenders may offer a "cosigner release" option after a certain period of on-time payments, but this is not guaranteed.

-

What happens to my credit and the cosigner's credit if I miss a payment?

- A missed payment will negatively impact both your credit score and your cosigner's credit score, as the loan is reported on both credit reports. This can lead to a drop in scores and make it harder for both parties to obtain new credit or favorable terms in the future.

-

Are there ways to build credit without needing a cosigner?

- Absolutely! Common strategies include opening a secured credit card (which requires a cash deposit), taking out a credit-builder loan (where funds are held until repayment), or using services that report your on-time rent payments to credit bureaus. Becoming an authorized user on someone else's well-managed credit card can also provide an initial boost.