Key Takeaways

- A 50-point drop indicates a significant change in credit factors, often related to utilization, new accounts, or payment history.

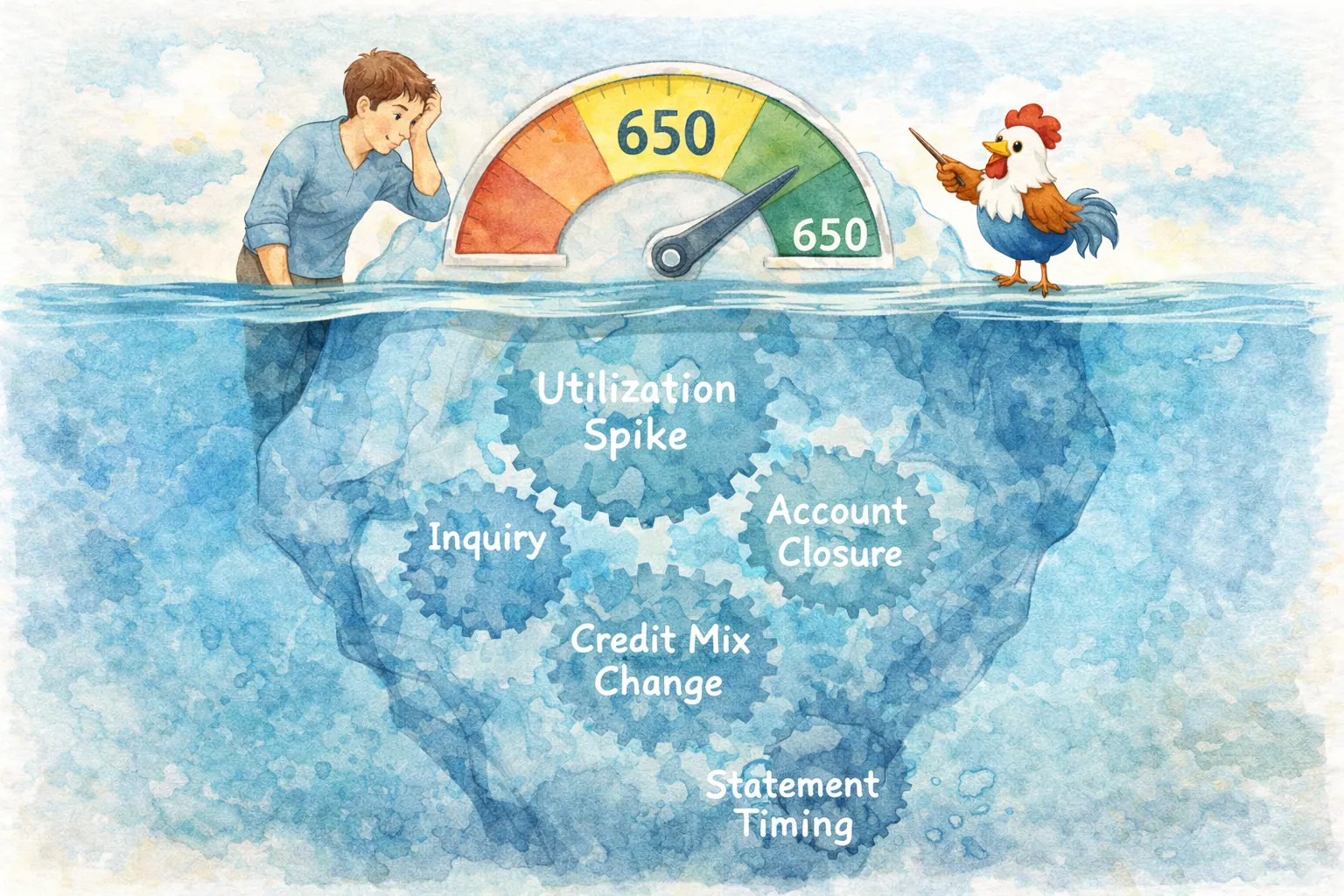

- Hidden reasons can include new inquiries, closed old accounts, becoming an authorized user on a troubled account, or unreported errors.

- The first step is always to get your free credit reports from all three bureaus to pinpoint the exact cause.

- Avoid quick fixes; a strategic, sequenced plan focusing on utilization, on-time payments, and building durable credit is essential.

- While AU tradelines may support short-term credit visibility for some profiles, long-term credit health still depends on your own consistent habits and account quality.

- Monitor your credit regularly to catch changes early and avoid preventable setbacks.

Quick Summary

A sudden 50-point credit score drop can feel alarming, but it is often a clear signal that one key credit factor changed. Identifying the exact cause, from utilization shifts to new inquiries or even identity theft, is the crucial first step to recovery.

Example Post-Drop Score Zone

The right response starts with diagnosis, not panic.

Real-Life Scenarios: How These Drops Play Out

Let us look at how these hidden reasons can impact people like Nico, the newcomer, and Riley, the rebuilder, and someone facing a time-sensitive financial need.

Nico's New Credit Jitters: Nico, proud of his 700+ score built from a single secured card and rent reporting, decided it was time to move into his own apartment. He applied for three apartments in quick succession, each requiring a credit check. The landlords, seeing multiple new hard inquiries from his applications and a slight increase in his secured card utilization (he bought some furniture), suddenly saw a 55-point drop. He learned that while he was doing well with building credit, rapid applications and slight utilization changes could cause temporary setbacks, especially with a still-thin credit file. This is where he could have benefited from ensuring his secured card balance was extra low before applying for the apartments, and spacing out applications where possible.

Riley's Unexpected Emergency: Riley had carefully nursed her credit score back up into the mid-600s after some past financial struggles. She had been keeping her two credit cards mostly clear, occasionally using one for gas and paying it off immediately. Then, her air conditioner broke in the middle of summer. She put the $2,000 repair bill on her card with a $2,500 limit. Even though she planned to pay it off with her next two paychecks, the high utilization (80%) was reported, and her score dropped by 60 points. This was a critical lesson: even temporary high utilization can cause significant damage, especially for rebuilders with lower credit limits.

The Home Buyer's Blunder: A couple, excited to buy their first home, had excellent credit scores. Just before closing, one spouse applied for a new store credit card to get a discount on appliances for their new home. The hard inquiry and the new account slightly lowered their score, but more critically, the lender re-pulled their credit just before closing. The 50-point dip, combined with an already tight debt-to-income ratio, nearly jeopardized their mortgage approval. They learned the hard way that it is crucial to avoid any new credit applications or significant financial changes in the months leading up to a major loan.

Your Credit Journey: A Lifelong Flight

Take control by checking your reports, identifying the cause, and following a clear plan. If you stay consistent across billing cycles, scores usually recover and become less volatile over time.

Pre-close balance review

Lower card balances 5-7 days before statements close.

Payment controls audit

Verify autopay, backup funding, and due-date reminders.

Three-bureau report check

Look for stale data, suspicious inquiries, and account errors.

Stability reset

If cash flow tightens, rebuild reserves before new credit actions.

This maintenance rhythm helps preserve gains after your score rebounds.

With patience and consistency, you are not just repairing short-term damage. You are building a stronger, more resilient profile that can better withstand future financial stress.

Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial, legal, or professional advice. Credit reporting practices and scoring models may change over time. Please consult a qualified professional for personalized guidance.

Frequently Asked Questions

1. What is the most common reason for a 50-point credit score drop?

- The most common reason for a sudden 50-point drop is a significant increase in credit utilization. Other frequent causes include new inquiries, late payments, or closure of an older account.

2. Can a single late payment cause a 50-point score drop?

- Yes. A payment reported 30+ days late can cause a large drop, especially if it is your first late mark, because payment history is heavily weighted in most scoring models.

3. How quickly can I recover a 50-point credit score drop?

- It depends on the cause. Utilization-driven drops can rebound faster after balances report lower. Late payments and inquiry clusters usually need more months of clean behavior.

4. Is a 50-point credit score drop normal?

- Small score movement is normal. A 50-point change is usually a meaningful signal tied to new debt pressure, a negative mark, or several recent inquiries.

5. What is the first thing I should do if my score drops?

- Pull and review all three reports (Experian, Equifax, and TransUnion) at AnnualCreditReport.com to identify the exact trigger before taking action.

6. Can checking my credit score too much lower it?

- No. Checking your own score is a soft inquiry and does not lower your score. Hard inquiries from new credit applications can cause temporary dips.

7. Do closed accounts hurt my credit score?

- They can. Closing an account can raise utilization and reduce average account age, both of which may pressure scores, especially on thinner files.