Key Takeaways

- Confirm all collection details (ownership, dates, bureaus) before any action to prevent mistakes.

- Understand that FICO 8 still penalizes paid collections, but FICO 9 and VantageScore treat them more favorably.

- Always negotiate 'pay-for-delete' in writing; settling for less than the full amount will be noted on your report.

- Paying a collection typically won't remove it from your report immediately, but it can reduce its negative impact over time.

- Focus on a holistic strategy that includes on-time payments, low utilization, and building new, positive accounts for lasting credit improvement.

- Monitor your credit reports carefully after any action to ensure accurate reporting across all three bureaus.

The Collection Shadow: Does Paying It Really Help?

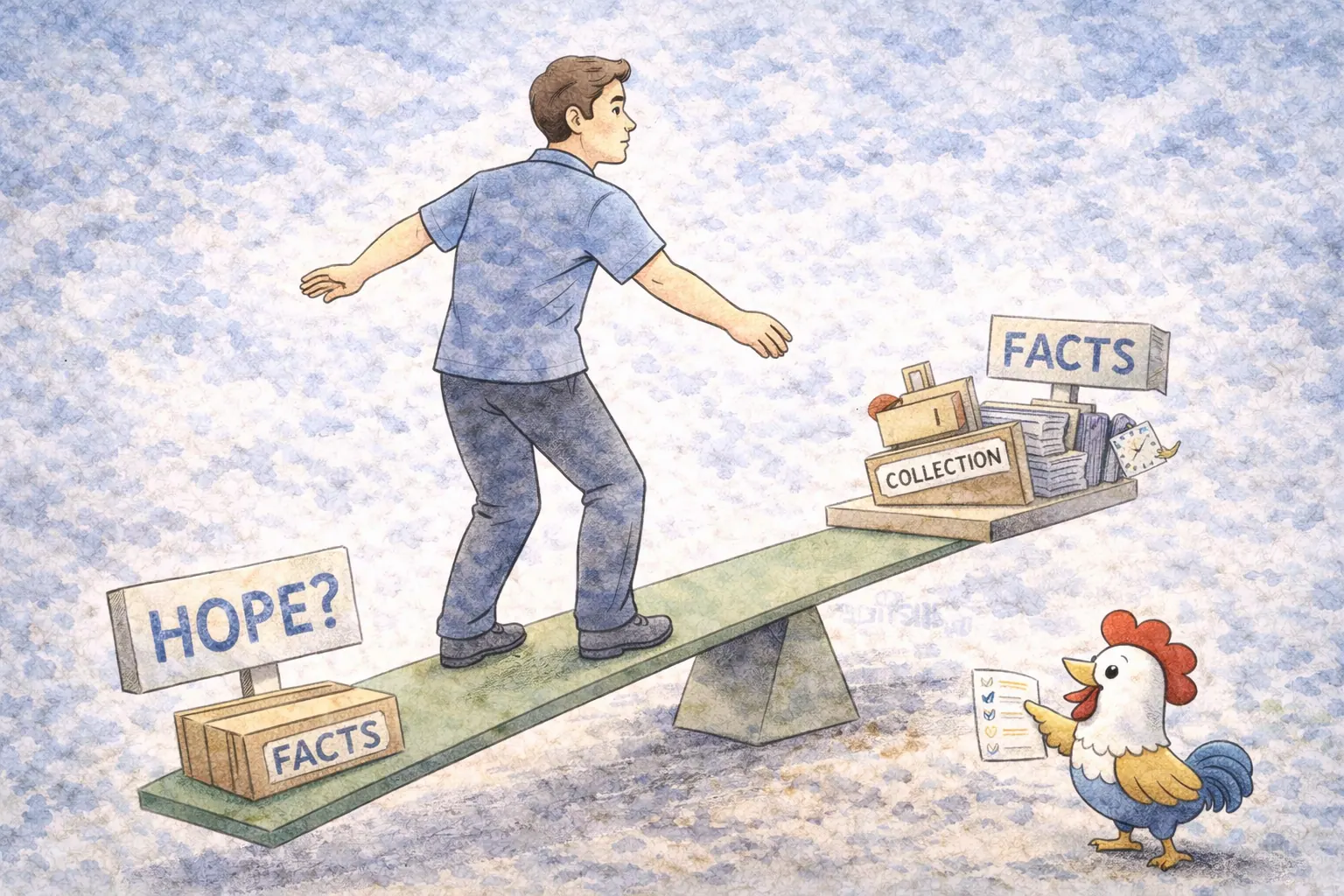

The direct answer is: Paying a collection can help your credit score, but it’s rarely a quick, magic bullet, and the impact depends heavily on the credit scoring model being used.

When a debt goes to collections, it means the original creditor has given up on trying to collect from you and sold the debt to a third-party collection agency. This event itself, the original account going to collections, causes significant damage to your credit score. The collection account then appears as a negative mark on your credit report for up to seven years from the date of the original delinquency, regardless of whether you pay it or not. This is a critical point that often surprises people.

Here’s where the nuance comes in: Different credit scoring models treat paid collections differently. Older models, like the widely used FICO Score 8, still view a paid collection account negatively, though typically less severely than an unpaid one. Think of it like a dark stain on your nest; even if you clean it, the residue might still be visible for a while. However, newer scoring models, such as FICO Score 9 and VantageScore 3.0 and 4.0, are more forgiving. They often ignore paid collection accounts entirely or give them significantly less weight, recognizing that you’ve fulfilled your obligation. This distinction is crucial because lenders use various scoring models, and you never know which one will be pulled when you apply for credit.

"Paying a collection account instantly removes it from your credit report and significantly boosts your score."

Paid collections can remain on your report for up to 7 years. Score impacts vary heavily by the exact scoring model used.

Why?

While paying is a responsible step, the damage from the original delinquency remains. Newer models ignore paid collections, but older ones still factor them in.

The Tricky Dance: Confirm, Document, Negotiate

Once confirmed, the next step is negotiation. Collection agencies often buy debts for pennies on the dollar, meaning they have a lot of room to negotiate. You might be able to settle the debt for less than the full amount. However, the golden standard is a "pay-for-delete" agreement.

Pay-for-delete

A negotiation where a collection agency agrees, in writing, to remove a collection account from your credit report entirely in exchange for payment. This is a strategy to remove negative entries from your credit report, though not all agencies will agree to it.

This is where the collection agency agrees, in writing, to remove the collection account from your credit report entirely once you pay. While collection agencies are not obligated to agree to this, and many won't, it's always worth asking. If they agree, get it in writing before you pay. A verbal promise is worthless. If they won't agree to pay-for-delete, negotiate a settlement that clearly states the account will be reported as "paid in full" or "settled for less than the full amount." A "paid in full" notation is generally better for your score than a "settled" notation.

The Impact on Your Credit Nest: What to Expect

Understanding the various scoring models is paramount to managing your expectations after paying a collection. Your credit nest is analyzed by different architects, and each has its own blueprints.

FICO 8 and Older Models: For years, FICO 8 has been the dominant scoring model, and under this system, a collection account, even a paid one, remains on your report and continues to negatively affect your score. The damage from the original delinquency is already done. While a paid collection is slightly better than an unpaid one, it doesn't remove the negative entry. Think of it as having an old, broken branch in your nest; even if you tape it up (pay it), it's still not a strong, new branch. The collection will eventually fall off after seven years from the date of the original delinquency, but paying it doesn't speed up that clock.

FICO 9 and VantageScore 3.0/4.0: These newer models offer a ray of hope. FICO 9, released in 2014, treats paid collection accounts much more favorably, often ignoring them when calculating your score. Similarly, VantageScore models also give less weight, or even no weight, to paid collections. If the lenders you're applying to use these newer models, paying off a collection could lead to a more noticeable score improvement. This distinction is critical because it means the same action can have different results depending on who's pulling your credit report. This variability underscores why it's so important to track score and reporting updates after each step across all bureaus.

Severity and Age: The impact of a collection account also depends on its severity and age. A newer, larger collection will typically have a more significant negative impact than an older, smaller one. As collections age, their impact on your score naturally diminishes, even if they remain on your report. If a collection is nearing its seven-year reporting limit, the boost you might get from paying it could be minimal, especially if other negative items are present.

Beyond Collections: Building a Stronger Nest (Durable Growth)

Addressing collection accounts is a crucial step in cleaning up your credit profile, but it’s just one branch of your overall financial nest-building strategy. For truly durable credit growth, you need to cultivate a broader range of healthy habits and accounts. After navigating the complexities of collections, your focus should shift to the foundational elements that build long-term credit strength.

First and foremost are on-time payments. This is the sturdy trunk of your credit nest. Every single on-time payment you make reinforces your reliability and positively impacts your score more than almost any other factor. Next is credit utilization, which refers to how much of your available credit you're using. Keeping this below 30% (and ideally below 10%) is like keeping your nest tidy and not overflowing, signaling responsible credit management. A healthy credit mix (a blend of revolving credit like credit cards and installment loans like car loans) and the age of your credit accounts also contribute to a robust profile.

For newcomers and rebuilders looking for a faster gateway to credit visibility, authorized user (AU) tradelines can be an effective initial step. By being added as an authorized user to an existing account with a long, positive history, you can quickly gain a boost to your credit age and utilization. While AU tradelines are a powerful starting point, remember that durable strength comes from adding your own accounts. This is where secured credit cards and credit-builder loans come into play. These tools allow you to demonstrate your own responsible borrowing and payment habits, building your unique credit history brick by brick. Rent reporting is another fantastic way to turn an existing monthly payment into a positive credit builder. These are the strong, self-made branches that will truly fortify your nest.

Resolve Collection

Add Positive Builder

Keep Utilization Low

Build Clean History

Your Action Plan: Step-by-Step

Taking control of collection accounts requires a methodical approach. Here’s a concise action plan to guide your efforts:

Action Items

This structured approach minimizes risk and maximizes the potential positive impact on your credit score, ensuring you are building your nest with intention.

Why Your Credit Score Truly Matters

While dealing with collections can feel like an isolated financial battle, it’s important to remember the bigger picture: your credit score is more than just a number. It's a reflection of your financial reliability and can open or close doors to significant life opportunities. A healthy credit score affects everything from the interest rates you qualify for on a car loan or mortgage to your ability to rent an apartment, get approved for utilities without a hefty deposit, and even secure certain jobs. It’s the invisible hand guiding many financial interactions, and neglecting it can lead to higher costs and fewer options.

So, does paying a collection increase your credit score? The truth is, it’s not a simple yes or no. It’s a strategic act that, when performed correctly and in conjunction with understanding how credit models work, can indeed help repair your credit nest. It’s about being informed, negotiating wisely, and then consistently layering positive habits.

Don't let the shadow of a collection paralyze you. Take informed action, build a strong foundation of on-time payments and low utilization, and explore powerful gateways like authorized-user tradelines to gain quick visibility. Then, shore up your nest with durable builders like secured credit cards and credit-builder loans. With patience and a clear strategy, you can turn a past stumble into a stepping stone toward a robust, thriving financial future. Your credit nest can, and will, become the sturdy sanctuary you deserve. Remember, we’re here to help you build your credit the right way, offering quick clarity now and durable credit growth next.

Disclosure

CreditRoost provides educational resources. We are not a credit repair organization, and we do not provide legal or financial advice. We cannot guarantee specific improvements to your credit score or the removal of accurate, negative information.

Frequently Asked Questions

1. Will a collection ever disappear from my credit report?

- Yes, collection accounts, whether paid or unpaid, will typically fall off your credit report after seven years from the date of the original delinquency, as mandated by the Fair Credit Reporting Act (FCRA). Paying the collection does not shorten this seven-year period.

2. Is 'pay for delete' a myth?

- 'Pay for delete' is not a myth, but it's also not guaranteed. It's a negotiation where a collection agency agrees to remove the collection entry from your credit report in exchange for payment. Many agencies will refuse, but it's always worth asking for it in writing before making any payment. Without a written agreement, there's no assurance the collection will be removed.

3. How long does it take for my score to improve after paying a collection?

- The time it takes for your score to improve after paying a collection varies. Once the collection agency reports the account as paid (which can take 30-60 days), newer scoring models like FICO 9 and VantageScore may adjust your score relatively quickly by giving less weight to paid collections. However, older models like FICO 8 still view paid collections negatively, so the impact might be minimal or take longer as the collection ages on your report.

4. Should I pay a collection if it's very old?

- If a collection is very old (e.g., nearing its seven-year reporting limit), the impact of paying it on your credit score might be minimal. However, it's still crucial to confirm the debt's validity and the statute of limitations in your state. Paying an old debt could 're-age' it, making it appear newer and potentially restarting the clock for legal collection efforts, even if it won't restart the credit reporting period. Assess if the payment is required for a specific loan approval or if you're better off letting it age off naturally while focusing on other credit-building strategies.

5. What if I can't afford to pay the full amount?

- If you can't afford to pay the full amount, you can often negotiate to settle the debt for a lower amount. Collection agencies frequently buy debts for less than their face value, giving them room to compromise. Always get any settlement agreement in writing, specifying the amount, the payment schedule, and how the account will be reported to the credit bureaus (e.g., 'settled for less than the full amount'). While a 'paid in full' status is generally better for your score, a 'settled' status is still preferable to an unpaid collection.

6. What's the difference between a charge-off and a collection?

- A charge-off occurs when an original creditor (like a bank) writes off a debt as uncollectible after you've missed payments for an extended period, typically 180 days. The account is closed to future charges, but the debt is still owed. A collection account, however, happens when that charged-off debt is sold or assigned to a third-party collection agency, which then attempts to collect the debt from you. Both are severe negative marks on your credit report, but they represent different stages of a delinquent debt. For a deeper dive into this, check out Charge Off vs Collection: The 5 Costly Mistakes People Make.