Key Takeaways

- Always verify the debt's ownership, original date of delinquency, and reporting on all three bureaus first.

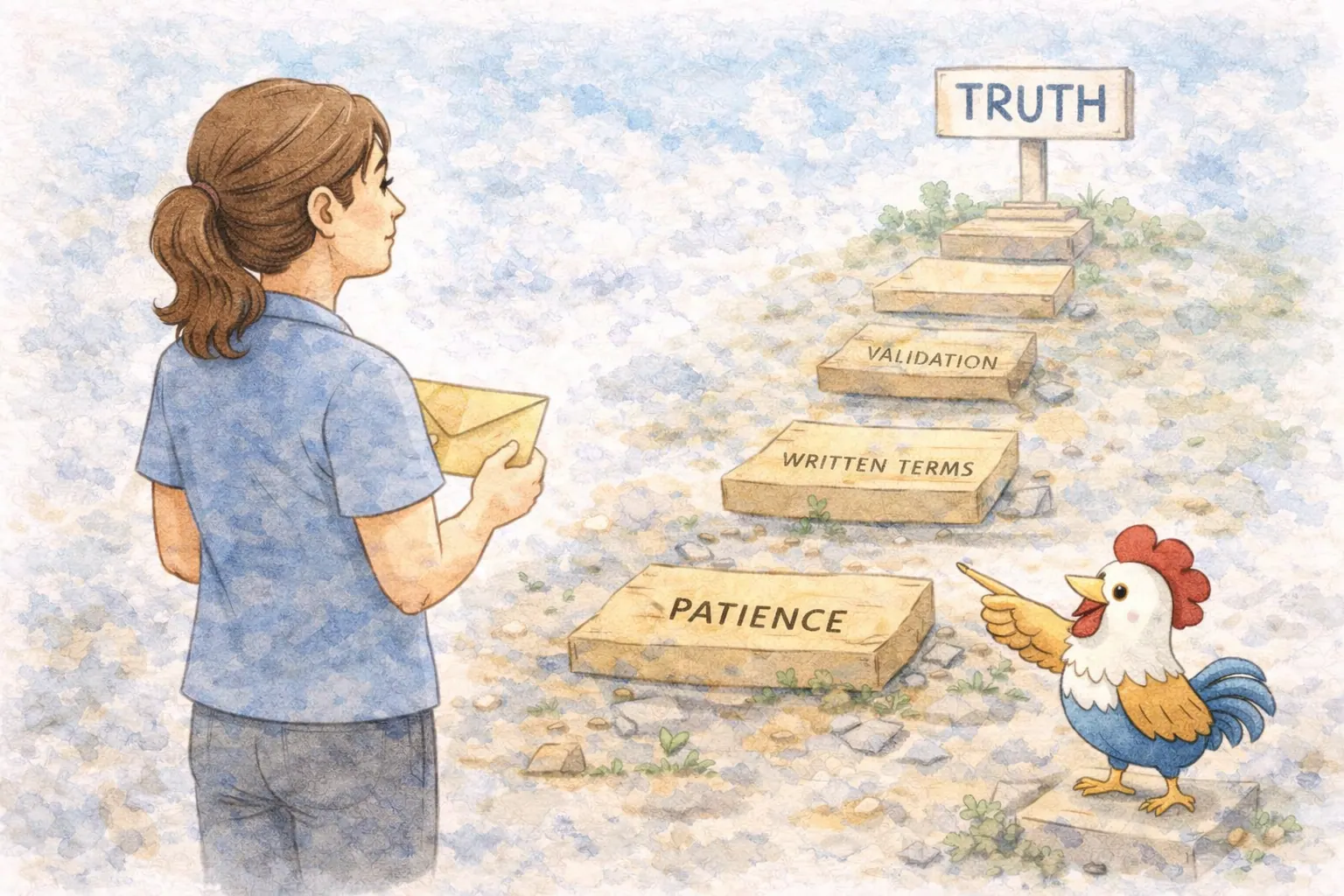

- Never pay a collection without a written 'pay for delete' agreement in hand that explicitly states deletion, not just an 'updated to paid' status.

- Negotiate for deletion, not just payment, and ensure the terms are documented and unambiguous.

- Document all communication and track credit score and reporting updates diligently across all bureaus after each step.

- Understand the statute of limitations and credit reporting limits in your state to avoid accidentally resetting the debt's age.

- Paying a collection without a deletion agreement can often just change its status to 'paid collection,' which remains a negative mark.

The Critical Steps You Must Take First

Before you even consider reaching for your wallet, there are foundational steps you must undertake. These aren't suggestions; they are non-negotiable pillars of a successful 'pay for delete' strategy, designed to protect you and your credit profile.

Pay for Delete

An agreement with a collection agency where you pay a debt in exchange for the agency completely removing the negative account from your credit reports, rather than just updating its status to paid.

First, Verify the Debt's Details. This is your reconnaissance mission. You need to know exactly what you're dealing with:

- Ownership: Is the collection agency contacting you the legitimate owner of the debt, or are they collecting on behalf of the original creditor? Request comprehensive debt validation. This forces the agency to prove the debt is yours and that they have the legal right to collect it. If they can't, they must remove it from your reports.

- Dates: What is the original date of delinquency (DOFD)? This is crucial because it dictates how long the collection can legally remain on your credit report, typically seven years from the DOFD, regardless of when it's paid. Paying an old debt can, in some cases, accidentally 'reset the clock' for certain scoring models, making it appear newer and potentially extending its negative impact. If the debt is old, check its statute of limitations before paying anything. This is one of the key mistakes highlighted in Should I Pay an Old Collection? 6 Mistakes to Avoid.

- Reporting: Pull your credit reports from all three major bureaus (Experian, Equifax, TransUnion). Is the collection account even on your reports? Sometimes an agency might claim a debt but hasn't reported it yet, or it's only on one or two bureaus. Knowing this helps you target your efforts effectively.

Second, and arguably the most vital step, is to Get Everything in Writing. In the world of credit repair, verbal agreements are as flimsy as spider silk. If an agent promises deletion over the phone, it means absolutely nothing without a documented, written agreement. This is where many people fall into the trap. No payment should ever be made without a letter explicitly stating that upon receipt of payment, the collection agency will remove the account from all three credit bureaus. The language must be clear: deletion, not just an 'update to paid' or 'cease reporting.' You need an ironclad commitment.

The Negotiation Dance: The Sequence That Matters

Navigating the world of collection agencies requires a strategic dance, where each step is carefully planned to avoid backfiring. Rushing in can turn your hopeful cleanup into a deeper mess. The sequence of your actions here is paramount.

Step 1: The Initial Dispute and Debt Validation Before you even utter the words 'pay for delete,' your first move is always to send a debt validation letter. This isn't just a courtesy; it's your right under the Fair Debt Collection Practices Act (FDCPA). This letter demands that the collection agency provide concrete proof that the debt is yours, the original amount, and that they have the legal authority to collect it. If they cannot validate the debt within 30 days, they are legally obligated to cease collection activities and remove any reporting of the debt from your credit file.

Step 2: Propose 'Pay for Delete' (If Validated) Only once the debt has been validated, and you've confirmed its legitimacy and that it's correctly reported, should you initiate the 'pay for delete' negotiation. Contact the agency (preferably in writing or via recorded line, followed by written confirmation) and state your willingness to pay a portion of the debt (or the full amount, if that's your strategy) in exchange for the complete deletion of the account from all three credit bureaus. Remember, collection agencies often purchase debts for pennies on the dollar, giving them significant room to negotiate. Don't be afraid to offer less than the full amount initially.

Step 1

Confirm ownership, balance, and dates before discussing payment.

Step 2

Ask for deletion, not just an update to paid status.

Step 3

Do not send money until the agreement is explicit and documented.

Step 4

After payment, monitor all three bureaus and follow up fast if deletion stalls.

Why Rushing Backfires (and Real-World Scenarios)

Let's paint a clearer picture of how failing to follow these steps can unravel your efforts, often leaving you worse off than before.

These scenarios highlight the payment trap. Collection agencies are in the business of collecting money, and they are masters of veiled promises. A 'paid collection' is still a negative item. Your ultimate goal must be deletion, not just payment, to truly clear that thorny branch from your credit nest. You want the account removed as if it never existed, rather than merely updated to reflect payment.

-

Nico, the Newcomer: Nico, eager to build his first credit nest, discovers a small, year-old medical collection on his report for $200. Frustrated, he immediately calls the agency, pays the full amount over the phone, and gets a verbal assurance that 'it'll be taken care of.' Weeks later, his credit score barely budges. When he checks his report, the collection still shows, but now its status reads 'Paid Collection.' While technically 'paid,' this entry still carries a significant negative weight, and Nico has lost his $200 with no credit benefit beyond a slightly updated status. He made the biggest mistake: paying without a written deletion agreement.

-

Riley, the Rebuilder: Riley, who's been diligently rebuilding his credit after some past financial storms, decides to tackle an old cell phone bill collection from four years ago. He calls the agency, agrees to pay a settlement, and they tell him they'll 'mark it paid.' Riley, relieved, makes the payment. What he didn't realize is that by making a payment on an older debt, he inadvertently acknowledged the debt. In some states and for some scoring models, this act can inadvertently reset the 'date of last activity' or even the statute of limitations, making the debt appear newer and potentially keeping it on his credit report for longer, or even allowing the agency to sue for collection again! His good intention became an accidental setback, as detailed in the pitfalls of Charge Off vs Collection: The 5 Costly Mistakes People Make.

Monitoring and What to Do If They Don't Comply

Once you’ve successfully navigated the negotiation, secured your written 'pay for delete' agreement, and made your payment, your work isn’t entirely done. This is where meticulous monitoring comes into play.

What if they don't delete?: If, after 45 days, the agreed-upon deletion hasn't occurred, it's time to act. Don't panic, but be firm and persistent. Send a certified letter to the collection agency, referencing your written 'pay for delete' agreement, the date of payment, and proof of payment (e.g., a copy of the cleared check or payment confirmation). Politely but firmly remind them of their contractual obligation.

If they still fail to comply, your next step is to dispute the collection directly with the credit bureaus. Attach copies of your written 'pay for delete' agreement and proof of payment as evidence. The bureaus are legally obligated to investigate your dispute within 30 days. Having a clear, written agreement makes your case undeniable.

Deletion Follow-Up Window

Check all three bureaus about 30 to 45 days after payment. If the account still appears, send a certified follow-up and be prepared to dispute with your written agreement.

Beyond Pay for Delete: Building Your Sturdy Nest

Successfully managing a collection account and securing a 'pay for delete' is a significant victory on your credit journey. However, it’s crucial to remember that this is just one piece of the larger puzzle. A sturdy, resilient financial nest isn't built on removing thorns alone; it also requires weaving in strong, healthy branches and habits.

-

Start with Visibility: For newcomers to the US credit system or those with very thin files, establishing a positive credit history quickly is often the first hurdle. An authorized user tradeline can provide a swift gateway to credit visibility, adding a seasoned account with positive payment history to your report. This can provide the initial lift needed to qualify for other credit-building products.

-

Add Durable Builders: While tradelines offer speed, true, lasting strength for your nest comes from your own accounts and habits. Incorporate reliable, self-managed credit builders like secured credit cards, which help you build credit responsibly with a security deposit. Consider a credit-builder loan, where you save money while making payments that build your credit history. And don't forget the power of rent reporting, turning an existing monthly expense into a credit-building asset.

-

Reinforce with Habits: The strongest nests are supported by consistent care. This means always making your payments on time, keeping your credit utilization low (ideally under 30%, but lower is better), and allowing your positive accounts to age gracefully. This combination of strategic problem-solving and diligent habit-forming is how you transform your financial profile from vulnerable to robust.

Your Path Forward: Building a Resilient Financial Roost

Dealing with collection accounts can feel daunting, like facing a formidable financial storm. But by understanding the biggest mistake people make before paying for delete: failing to verify and secure a written-agreement, you've armed yourself with crucial knowledge. Remember, patience, verification, and documentation are your most-powerful allies.

Don't rush, don't assume, and never pay a penny without that explicit, written 'pay for delete' agreement in hand. Your efforts will be rewarded with a cleaner credit report and a healthier financial future.

Action Items

Frequently Asked Questions

1. What exactly is a 'pay for delete' agreement?

- A 'pay for delete' is a negotiation with a collection agency where you agree to pay a certain amount (often less than the full debt) in exchange for them completely removing the collection account from all your credit reports. The key is deletion, not just updating the status to 'paid.'

2. Why is it so important to get a 'pay for delete' agreement in writing?

- A written agreement is crucial because verbal promises from collection agencies are often not honored. Without a document explicitly stating deletion upon payment, you risk paying the debt only to have it remain on your report as a 'paid collection,' which still negatively impacts your score.

3. What critical details should I verify about the debt before attempting a 'pay for delete'?

- You should verify the debt's ownership by the collection agency, the original date of delinquency (DOFD) to understand its age and reporting limits, and whether it's currently being reported on all three major credit bureaus (Experian, Equifax, TransUnion).

4. Can paying an old collection debt accidentally harm my credit score or reset the clock?

- Yes, in some cases, paying an old collection, especially without a deletion agreement, can inadvertently reset the 'date of last activity' or even the statute of limitations. This can make the debt appear newer on your credit report and potentially extend its negative impact or even allow the agency to sue for collection again.

5. What should I do if a collection agency refuses to provide a written 'pay for delete' agreement?

- If an agency refuses to provide a written 'pay for delete' agreement, it's generally best not to pay them. You might explore other options, such as letting the debt age off your report if it's nearing the seven-year reporting limit, or focus on other credit-building strategies.

6. What steps should I take if a collection agency doesn't delete the account after I've paid and have a written agreement?

- If the account is not deleted after 30-45 days, send a certified letter to the collection agency referencing your written agreement and proof of payment. If they still don't comply, dispute the collection directly with all three credit bureaus, providing your written 'pay for delete' agreement as undeniable evidence.

Disclosure

CreditRoost provides educational resources. We are not a credit repair organization, and we do not provide legal or financial advice. We cannot guarantee specific improvements to your credit score or the removal of accurate, negative information.