Key Takeaways

- Dedicate monthly savings towards specific, known future expenses like car repairs, holidays, or home upgrades.

- Label your funds clearly (e.g., 'Car Maintenance,' 'Vacation,' 'Holiday Gifts') to stay organized and motivated.

- Avoid credit card debt for large, predictable costs by having cash ready when these expenses arise.

- Integrate sinking funds into your overall budget, complementing your emergency fund and regular savings.

- Consider using a high-yield savings account to house your sinking funds, allowing your money to grow slightly while it waits.

The Why Behind the Nest Egg

You might be thinking, "Isn't that just saving?" At its core, yes. But this is saving with intention, specificity, and a strong psychological edge. Unlike a general savings account, which can feel vague, a sinking fund is earmarked. It has a purpose, a target, and a timeline.

The real value of this system is how it reduces reliance on high-interest credit during predictable spikes. When a major expense is coming and you have already saved for it, you avoid putting it on a credit card and adding interest. That proactive approach gives you more flexibility and peace of mind, and it strengthens the overall stability of your financial nest.

Sinking Fund

A dedicated savings bucket for a predictable future expense, with a target amount and a target date.

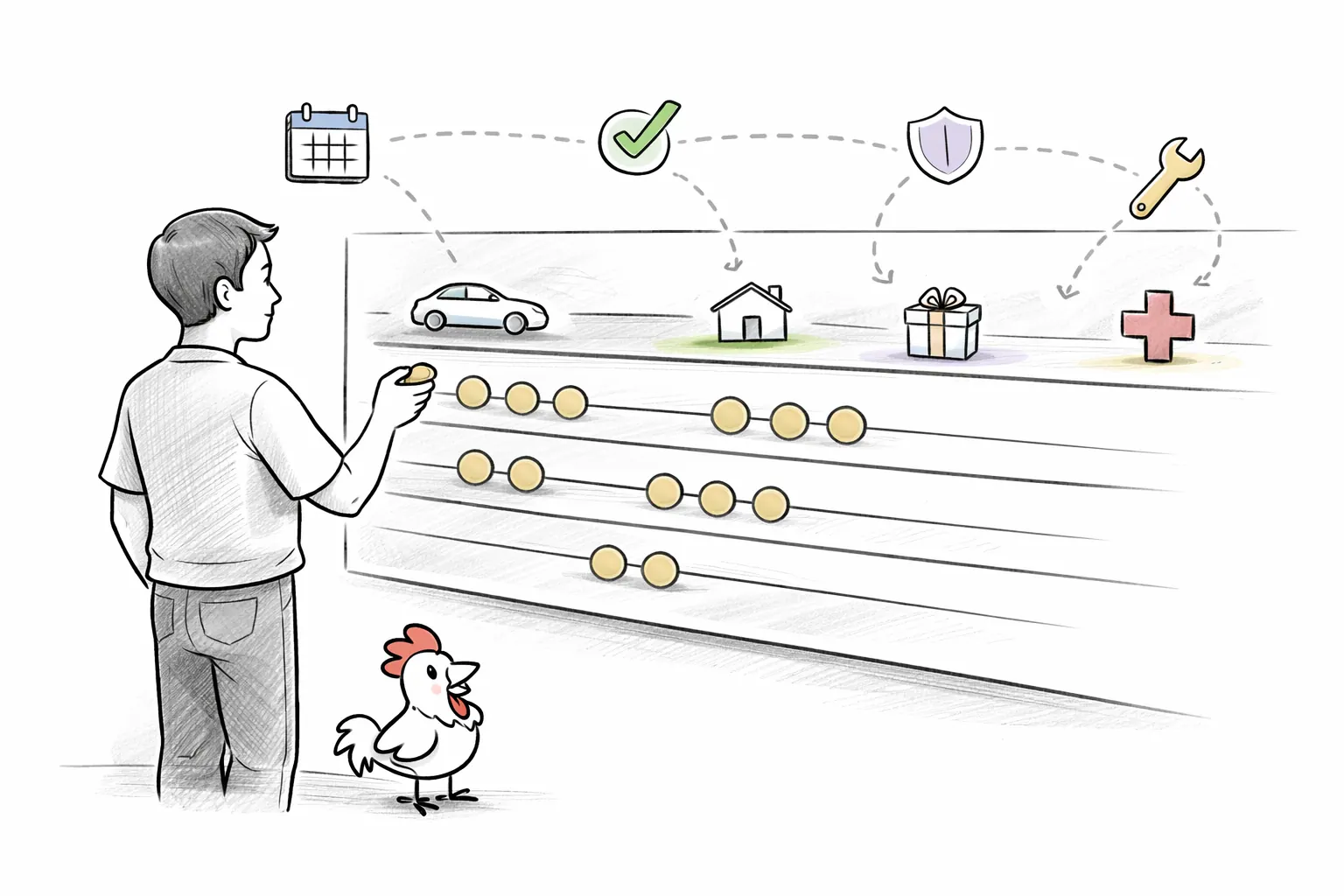

Hatching Your Funds: A Step-by-Step Guide

First, identify your known future expenses. These are the costs that you anticipate will pop up within the next year or two. Think about:

- Annual or Semi-Annual Bills: Car insurance, property taxes, professional memberships.

- Regular Maintenance: Car repairs (tires, oil changes, inspections), home maintenance (roof cleaning, HVAC service).

- Events and Celebrations: Holiday gifts, birthdays, anniversaries, weddings, family vacations.

- Planned Purchases: A new appliance, furniture, electronic upgrades, a down payment on a larger purchase.

This simple monthly pacing is what turns a large bill into a manageable cash payment.

Is this expense predictable and due within 12-24 months?

This quick filter helps you decide where each dollar belongs before a due date creates pressure.

Weaving Funds into Your Financial Nest

Integrating sinking funds into your overall financial picture makes your budget feel less restrictive and more empowering. If you follow a system like the 50/30/20 rule, your sinking fund contributions would typically come out of your 'Savings & Debt Repayment' (the 20%) category. Instead of seeing that 20% as just one lump sum, you can break it down further: a portion for your emergency fund, a portion for retirement, and specific amounts for each of your sinking funds.

The exact percentages can shift by season, but assigning each dollar to a clear lane is what keeps the plan stable.

For example, if your 20% savings slice is $500 per month, you might allocate $100 to your emergency fund, $200 to retirement, $100 to a 'Vacation Fund,' and $100 to a 'Home Repair Fund.' This granular approach gives every dollar a job, making your financial planning incredibly precise and preventing money from 'disappearing' into general savings without a purpose.

This deliberate allocation strengthens your financial nest in multiple ways. You avoid debt for these expenses and gain a clearer understanding of where your money goes and what it’s working towards. It fosters a sense of control and foresight, turning potentially stressful financial moments into non-events because you’ve already prepared for them.

The Rewards and Realities of Sinking Funds

The benefits of adopting a sinking fund system are profound, extending far beyond simply having money for a big purchase:

- Debt Avoidance: This is perhaps the most significant advantage. By proactively saving, you sidestep the need to use credit cards, personal loans, or other high-interest debt instruments for predictable expenses. This can help protect your score by limiting spikes in credit utilization, can support a cleaner payment history, may save you money on interest, and can keep more of your hard-earned cash in your pocket. If predictable costs have already become balances, pair your plan with Negotiating with Creditors while rebuilding savings momentum.

- Reduced Financial Stress: Knowing you have money set aside for upcoming expenses brings immense peace of mind. No more dreading holiday season bills or worrying about how you'll afford that annual car service. You're prepared, calm, and confident.

- Goal Achievement: Sinking funds are powerful tools for achieving specific goals. Want to travel? Save for a down payment on a new home? Fund a child's education? Labeling a fund for that goal makes it tangible and achievable.

- Better Budget Adherence: When you have money specifically earmarked, you’re less likely to overspend in other areas because you know those funds have a vital purpose.

Sinking Fund Discipline Rules

- Keep each fund labeled and separate

- Automate contributions on payday

- Recalculate monthly targets when costs change

- Borrow from one fund for unrelated spending

- Treat sinking funds like emergency cash

- Ignore annual bills until they are due

Following these basics keeps your system practical and prevents small leaks from breaking your plan.

While the system is strong, it is not without challenges. The primary risk is a lack of discipline. If you keep borrowing from sinking funds for unrelated spending, the system breaks down. It takes commitment and consistency, like any financial habit. Another misconception is that sinking funds are a quick way to build wealth. They are not. They are a disciplined way to manage predictable expenses, not a shortcut to rapid growth. Still, with steady effort, they can contribute to a stronger and less stressful financial life.

Real-Life Nests: Sinking Funds in Action

Let's bring this system to life with a few familiar scenarios:

-

Nico, the Newcomer, and the Appliance Upgrade: Nico, having just secured his first apartment, is working on building his financial nest. He’s got his emergency fund started, and he knows that within the next year, he'll want to replace his old, hand-me-down washing machine. A decent new one will cost about $800. He decides to open a 'New Appliance' sinking fund. With 10 months until he plans to buy it, he sets up an automatic transfer of $80 each month from his checking account into this dedicated savings pot. When the time comes, Nico can confidently purchase his new machine with cash, without touching his emergency fund or putting a significant expense on a credit card he's still carefully using to build positive history with a secured card. This makes his journey toward financial stability feel secure and empowered.

-

Riley, the Rebuilder, and Annual Property Taxes: Riley has diligently worked to rebuild her credit and stabilize her finances after a tough period. One recurring headache has always been her annual property tax bill, which totals $3,600 and is due every October. In the past, this large sum would put a strain on her budget, sometimes leading to late payments or having to put it on a credit card, hindering her progress. This year, Riley decides to implement a 'Property Tax' sinking fund. Starting in November after the previous bill, she divides $3,600 by 11 months (until the next October payment). She sets up an automatic transfer of $327.27 each month. By the time October rolls around, her 'Property Tax' egg is full, and she pays the bill with ease, feeling the profound relief of being financially prepared, rather than stressed.

-

The Time-Sensitive Family Vacation: A family of four plans a much-anticipated vacation next summer, estimated to cost $4,000 for flights, accommodation, and activities. They have 12 months to save. Rather than hoping for a bonus or draining their main savings right before the trip, they create a 'Vacation Fund.' They set up an automatic transfer of $333.33 each month. This dedicated fund ensures that when summer arrives, the trip is fully paid for, allowing them to enjoy their time without the shadow of impending debt or the worry of depleting their emergency reserves. They return home refreshed, not financially depleted.

Set target and deadline

Define the total amount and due date for each planned expense.

Automate contributions

Transfer the monthly amount right after payday.

Review and adjust

Recalculate if prices changed or the due date moved.

Pay in cash from the fund

Cover the expense without draining emergency savings or adding new debt.

Seeing the flow over time keeps the strategy practical and easier to repeat for the next goal.

Your Sinking Fund Action Plan

Ready to build out your own series of sinking funds? Here's a simple, actionable plan to get started:

List known large expenses for the next 12-24 months

Estimate each cost and timeline, leaning slightly high when unsure

Calculate each monthly contribution (cost ÷ months until due)

Set up dedicated sub-accounts or clear trackers for each fund

Automate transfers on payday so contributions happen consistently

Review and adjust your targets as costs and timelines change

Use this as a living process, not a one-time setup. Separate tracking and regular reviews are what keep targets realistic and cash flow stable.

If you want a practical checklist behind these milestones, start by writing out your anticipated expenses for the next 12-24 months and think broadly, from holidays to repairs to annual memberships. Then estimate amounts and due dates, set up dedicated sub-accounts or trackers (including envelopes or a spreadsheet if that works better for you), and Automate Your Transfers on payday so the plan runs consistently. Finally, revisit your funds every few months, adjust contributions when costs shift, and add new categories when goals change.

Cultivating a Resilient Financial Roost

Embracing the sinking fund system is a testament to mindful money management. It’s about being proactive, not reactive, with your finances. It transforms the stress of inevitable big purchases into a manageable, even empowering, part of your financial routine. By consistently setting aside a little bit each month, you're not just saving money; you're cultivating financial discipline, helping reduce future debt, and ultimately, building a more resilient and peaceful financial nest.

Key Standard to Follow

If an expense is predictable and recurring, plan for it with a sinking fund before it arrives. Reserve emergency savings for true surprises.

That distinction keeps both systems healthy and prevents you from draining the wrong account at the wrong time.

Disclosure

Savings and credit outcomes vary by individual profile, spending behavior, lender criteria, and scoring model. A sinking fund strategy may help reduce reliance on debt, but it does not guarantee loan approval, specific credit score changes, or underwriting outcomes.

Quick Sinking Fund Checklist

Use this as your recurring reset so your plan stays clean, current, and actionable.

Just as a wise bird meticulously gathers materials for each part of a nest, with strong twigs for the base, soft down for the lining, and specialized pieces for future repairs, you can build financial resilience with that same intention. The sinking fund system gives you a clear path to meet big purchases with "I've got this" instead of "How will I pay for that?" It is practical self-care for your financial future and helps keep your nest stable, calm, and ready for what comes next.

Frequently Asked Questions

- What is the main difference between a sinking fund and an emergency fund?

- An emergency fund is for unexpected events like job loss or medical emergencies, while a sinking fund is for known, predictable future expenses like vacations or car repairs.

- How do I decide which expenses need a sinking fund?

- Start by listing any large, non-monthly expenses you anticipate within the next 1-2 years that you don't want to put on a credit card or drain your main savings for. Common examples include holidays, car maintenance, property taxes, or annual insurance premiums.

- Do I need a separate bank account for each sinking fund?

- While not strictly necessary, using separate savings accounts (often available as sub-accounts with digital banks) or clearly labeling digital 'envelopes' is highly recommended. It provides psychological clarity and prevents accidental spending.

- How much should I contribute to each sinking fund monthly?

- Estimate the total cost of the expense and divide it by the number of months you have until the expense is due. For example, a $600 expense due in 6 months would require $100 per month.

- What if I don't use all the money in a sinking fund?

- If you oversave or an expense comes in under budget, you can reallocate the surplus to another sinking fund, boost your emergency fund, or contribute it to long-term savings or investments.

- Can I use a high-yield savings account for my sinking funds?

- Absolutely! A high-yield savings account is an excellent place to keep your sinking funds, as it allows your money to earn a bit of interest while it waits for its intended purpose, making your savings work harder for you.

- What's the biggest challenge with the sinking fund system?

- The biggest challenge is often discipline. Consistently contributing each month and avoiding the temptation to 'borrow' from a fund for an unrelated purpose is crucial for the system's success.