Key Takeaways

- Insurance helps turn a large unpredictable loss into a smaller predictable cost.

- Health, auto, and renters or homeowners coverage are often the first policies most households need.

- Deductibles, limits, and exclusions matter as much as the monthly premium.

- The right coverage can help keep a major emergency from turning into collections or new debt.

- Review coverage regularly as your income, assets, and responsibilities change.

Why Insurance Is a Financial Stability Tool

At the simplest level, insurance changes the shape of risk. Instead of facing one huge, unpredictable bill on your own, you pay a smaller and more predictable cost over time through premiums.

You still carry part of the cost. Deductibles, co-pays, uncovered losses, and even higher premiums after a claim can all still show up. But a well-structured policy can keep a large emergency from turning into a full financial reset.

The Real Goal

Insurance is not about chasing the cheapest premium. It is about keeping one serious loss from wiping out savings or forcing expensive borrowing.

Insurance sits alongside the rest of your protection layers. Your cash reserve handles smaller surprises. Your regular budget handles the usual bills. Insurance is there for the larger events that would otherwise hit harder than your monthly plan can absorb.

If you are still tightening your finances after a rough stretch, that distinction matters. One uncovered emergency can undo months of steady work. With better coverage, the same event may still be frustrating, but it is less likely to become a chain reaction that affects every other bill.

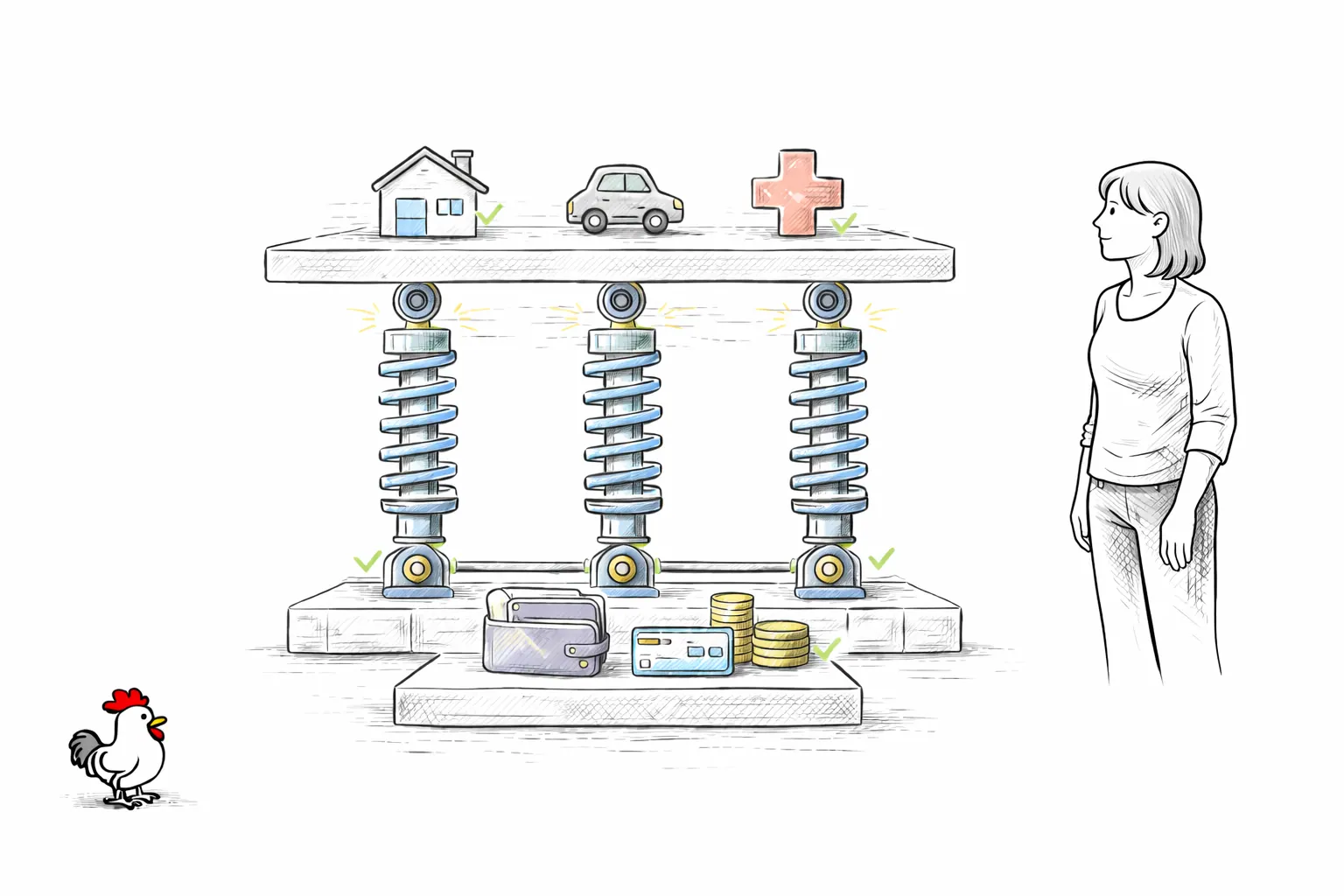

The Core Policies Most Households Should Understand

Few people need every type of insurance at once. What they do need is a clear handle on the core policies that carry most of the day-to-day financial weight.

Core Insurance Basics

| Coverage type | What it helps protect | Why it matters |

|---|---|---|

| Health insurance | Medical costs after illness, injury, or routine care | Large medical bills can overwhelm cash flow quickly. |

| Auto insurance | Vehicle damage and liability after covered accidents | A claim can involve repair costs, injuries, or legal liability. |

| Renters or homeowners | Personal property, liability, and housing-related losses | A fire, theft, or guest injury can create large replacement or liability costs. |

For health coverage, it also helps to know the practical cost-sharing terms. Co-pays are the fixed amounts you pay for certain visits or prescriptions, while the out-of-pocket maximum is the most you should pay in a plan year for covered care before the plan takes on more of the cost. Those details often decide whether a plan feels manageable in real life, not just on paper.

Auto insurance matters because the financial risk can go far beyond your own car. Damage to another vehicle, injuries to another person, towing, rental costs, and liability exposure can all come into play. Requirements vary by state, but the bigger issue is whether your limits are realistic for the type of loss you could face. If you hear someone say full coverage, they usually mean liability plus collision and comprehensive coverage, which can help pay for damage to your own vehicle after an accident, theft, vandalism, or certain non-collision losses.

Renters insurance and homeowners insurance are often underestimated because people focus only on the value of their belongings. The broader value is that these policies can also help with liability exposure and major property loss. Replacing clothes, electronics, furniture, or temporary housing after a serious event can be much harder than it sounds when you have to pay for it all at once.

You may add more specialized coverage later, but these three are usually where the most practical protection starts.

How Deductibles, Limits, and Exclusions Change the Real Cost

The premium alone does not tell you much. What matters is what happens when something actually goes wrong.

The premium is the recurring amount you pay to keep the policy active. That monthly or annual cost matters, but it only tells part of the story. A lower premium can still leave you exposed if the deductible is too high or the coverage is too thin.

Could you comfortably cover the deductible tomorrow without missing other important bills?

The second number is the policy limit. That is the maximum amount the insurer may pay for a covered loss. If your real cost is higher than the limit, the gap may become your responsibility.

Some policies also offer riders or endorsements. These are optional additions that expand protection for specific items or situations, such as expensive jewelry, business equipment, or other risks the standard policy handles poorly or not at all.

The piece many people miss is exclusions. Every policy has things it does not cover or situations where the payout is narrower than you expected. Saying "I have insurance" is not enough by itself. You need to know what type of event is covered, what conditions apply, and what amount you may still need to pay personally.

Deductible

The amount you pay out of pocket before insurance begins covering a covered loss. A higher deductible often lowers the premium but increases the cash you need during a claim.

A cheap policy can get expensive fast if it leaves too much risk on your side. A lower premium may still be the right choice, but only if the out-of-pocket exposure still fits your actual finances.

How Insurance Can Help Protect Your Credit

Insurance does not usually build credit directly, but it can help protect the conditions that keep your credit profile healthier.

Before a loss

The policy helps define how much risk you are keeping and how much risk you are transferring.

When a loss happens

Your deductible and uncovered costs still matter, but the insurer may absorb the larger share.

After the event

A smaller out-of-pocket hit can make it easier to stay current on loans, cards, and rent.

Longer term

A covered emergency is less likely to become collections, rushed borrowing, or a deeper financial setback.

Insurance also should not replace an emergency fund. The two tools do different jobs. Insurance can help with catastrophic or high-cost losses. Your reserve still helps with deductibles, immediate expenses, and the smaller gaps that policies do not fully cover.

How to Shop for Coverage Without Buying Blind

The best insurance decision is rarely the fastest one. It usually comes from comparing the parts of the policy that matter after a claim.

Start by comparing the same coverage structure across multiple quotes. If one price looks dramatically lower, check whether the deductible is higher, the limits are lower, or important details changed in the fine print.

Independent agents can be useful here because they can often compare multiple carriers for you. Online quote tools can help too, but the real value comes from making sure you are comparing the same structure each time instead of being pulled in by a lower headline number.

Focus on these questions:

Insurance Shopping Checklist

Look at policy fit, not just sticker price. A plan that looks affordable on paper may still be a bad fit if it leaves you underinsured in the areas most likely to disrupt your life. A slightly higher premium may be worth it if it gives you a more realistic deductible, stronger liability protection, or fewer painful gaps.

Bundling can help too. If the same insurer gives you a meaningful discount for combining auto and renters or homeowners coverage, that may lower total cost without cutting important protection. It also makes the admin side simpler, which helps once renewals, bills, and claims all start competing for your attention.

It is also worth asking about plain, unglamorous discounts. Safe-driver programs, anti-theft devices, good-student discounts, autopay, paperless billing, and certain home safety features can all lower premiums depending on the insurer. None of those should be the main reason you choose a policy, but they can reduce cost without forcing you to cut useful protection.

This is the time to understand the claims process before you ever need it. Keep policy numbers easy to find, know how to contact the insurer, and understand the basic steps for reporting a loss. It feels like routine admin work until the day it saves you time, stress, and expensive errors.

Regular reviews matter here. Coverage that made sense when your finances were thinner may not fit once your savings, responsibilities, or assets have grown. The reverse is also true: if money is tighter than it used to be, you may need a more realistic structure instead of pretending you could easily absorb a large deductible.

Building Insurance Into Your Monthly Plan

Insurance works better when it is treated like a core operating expense instead of an afterthought. If the premium feels optional each month, it becomes much easier to let a policy lapse or to underinsure yourself just to create short-term breathing room.

Put the premium inside your recurring monthly plan. Keeping the policy active matters, but the bigger job is keeping your protection aligned with the kind of financial stability you are trying to build.

In practice:

- Keep premiums inside your fixed-expense plan.

- Hold back enough savings to cover the deductible you chose.

- Reassess coverage after life changes instead of waiting for renewal notices to force the conversation.

- Make sure insurance decisions still match the rest of your risk management, including your savings and debt strategy.

Monthly Coverage Habits

- Treat premiums like a required bill inside your fixed expenses.

- Keep deductible cash separate so a claim does not derail rent or groceries.

- Review coverage when your income, housing, or vehicle situation changes.

- Assume a low premium automatically means the policy is affordable in a crisis.

- Let a policy lapse to create temporary breathing room without a backup plan.

- Wait until claim day to figure out what your deductible or exclusions actually are.

Once insurance is built into the system, it becomes easier to make calmer decisions during stress. You are not scrambling to figure out whether one accident means using a credit card, skipping a payment, or pulling money that was supposed to cover rent or groceries.

Other Types of Insurance Worth Considering

As your finances get more complex, the core policies may stop being the whole picture. Health, auto, and renters or homeowners coverage usually come first, but they are not the only kinds of protection that may matter over time.

A yearly review is a solid baseline, plus any major life change.

Disability insurance can replace part of your income if you cannot work because of illness or injury. For many households, income is the biggest financial asset they have. If that paycheck disappears for months, the pressure can spread fast through savings, debt, and every fixed bill.

Life insurance becomes more important when other people rely on your income or when large debts would burden someone else if you died. For many households, term life insurance is the clearest and most affordable starting point because it covers a specific period when the financial risk is highest. Whole life insurance is different: it is usually more expensive, lasts for life, and may include a cash-value feature. That can fit some plans, but it is a separate decision from the simple question of whether your household needs protection first.

Long-term care insurance is a later-stage planning tool, but it matters because extended care can become extremely expensive and can drain savings faster than many families expect. It is not an urgent priority for everyone, but it belongs in the larger insurance conversation as responsibilities and assets grow.

You do not need every policy available. Start by identifying which risks would do the most damage to your household, then add protection in a deliberate order as your life changes.

How Insurance Fits Into Your Bigger Financial Plan

Insurance is one layer of protection, not the whole system. It works best next to cash reserves, routine budgeting, and realistic debt management instead of trying to replace them.

That is why many people treat the emergency fund and insurance as separate jobs inside the same system. Your reserve may cover a few months of living costs or smaller urgent bills. Insurance is what keeps a five-figure or six-figure event from wiping that reserve out in one hit.

Risk tolerance matters here too. Some people prefer higher deductibles and lower premiums because they have a stronger cash cushion. Others would rather pay more each month for a lower deductible and less uncertainty when a claim happens. Neither choice is automatically right. The better choice is the one that fits your real reserves, not the one that only looks cheaper on paper.

Frequently Asked Questions

1. What insurance should most people prioritize first?

- Health insurance, auto insurance if you drive, and renters or homeowners coverage usually handle the most common high-cost risks for most households.

2. Is the cheapest premium usually the best choice?

- Not by itself. A cheaper premium can still be expensive if the deductible is too high, the limits are too low, or the policy leaves major gaps you cannot afford.

"The cheapest premium is automatically the smartest policy."

A stronger fit usually matters more than the lowest monthly price.

Why it matters

If the deductible is unrealistic or the exclusions are too broad, a low premium can still leave you paying the painful part of the loss yourself.

3. How does insurance help my credit if it does not report to the bureaus?

- It can reduce the odds that a major emergency turns into new debt, missed payments, or collection pressure that then damages your credit habits and cash flow.

4. Can my credit score affect my insurance rates?

- In many states and for some policy types, yes. Some insurers use credit-based insurance scores as part of their risk model, which means stronger credit can sometimes help lower premiums.

5. Is renters insurance worth it if I do not own much?

- Usually, yes. It is not only about replacing belongings. Renters coverage can also help with liability and other costs that are much harder to absorb out of pocket all at once.

6. What is the difference between liability and full coverage auto insurance?

- Liability coverage helps pay for damage or injuries you cause to other people or their property. Full coverage usually means liability plus collision and comprehensive coverage, which can also help pay for damage to your own vehicle under covered situations.

7. What is an umbrella insurance policy?

- An umbrella insurance policy adds extra liability protection above the limits on your auto, renters, or homeowners policy. It can matter if you have growing assets, a higher income to protect, or simply want a larger buffer against a serious lawsuit.

8. Should I choose a high deductible to save money every month?

- Only if the deductible still fits your real emergency cash position. A lower premium is not much help if a claim would immediately force you into borrowing.

9. How often should I review my coverage?

- At least once a year and after major changes such as moving, buying a vehicle, taking on new responsibilities, or building more savings and assets.

10. Are there practical ways to lower premiums without stripping out too much coverage?

- Sometimes. You may be able to lower costs by comparing quotes regularly, bundling policies, adjusting deductibles carefully, asking about discounts, using safety features, and keeping your credit and claims history healthier over time.

A good insurance decision usually feels uneventful before you need it. That is the point. The policy is there so one bad event does not get to rewrite the rest of your financial plan.

When coverage, savings, and budgeting work together, a setback is more likely to stay temporary instead of becoming a longer debt problem.